August 2019 - Market Update

/Monthly Update || August 2019

“There are two kinds of people who lose money: those who know nothing and those who know everything.”

Opening Remarks

First a quick note: we hosted our third quarterly conference call on July 16th. The replay can be found here. We had 150 people from around the world dial-in, and the replay has been streamed more than 1,000 times. We are honored by that response and invite you to listen if you haven’t already. Now on to the main event!

Greetings from inside Ikigai Asset Management1 headquarters in Marina Del Rey, CA. We welcome the opportunity to bring to you our eleventh Monthly Update and hope these are helpful in better understanding some of what we’re doing and what we’re seeing. We have the privilege of deploying capital on behalf of our investors into a new technology and asset class that we believe will fundamentally change the world and create trillions of dollars of value in the process.

We believe we are obligated to be shepherds of this technology – to help the world better understand the powerful potential of DLT and crypto assets, and to fund and be an ambassador for DLT projects that will change our lives forever.

To that end, July was nothing short of historic for Bitcoin and crypto as a whole. In a single seven day stretch, 1) The Chairman of the Fed testified to Congress about it; 2) The President tweeted about it; 3) The Treasury Secretary gave a formal press conference about it; and 4) Congress questioned a Facebook executive and other crypto ecosystem participants for two days about it… Take a step back and think about that sentence. There is a good chance that crypto will become a key topic in the 2020 presidential debates…Take a second and think about that one too. What a time to be alive!

The news cycle around these events was enormous. Bitcoin, Libra and cryptocurrency were discussed on every major news outlet and in every major publication. The media, casual observers and crypto ecosystem participants generated the full spectrum of reactions – from bullish to bearish to uncertain. Much of the disparity in those reactions was the product of the disparity in views from the politicians that discussed them. Jay Powell called Bitcoin a speculative store of value. Trump said he was not a fan. Mnuchin said speculating on Bitcoin on regulated exchanges was fine. Rep. Brad Sherman compared crypto to 9/11. Rep. Patrick McHenry called Bitcoin an unstoppable force. Rep. Warren Davidson differentiated between Bitcoin and shitcoins.

Given that array of reactions from politicians, it should come as no surprise that the analyses of these reactions by market participants were mixed as well. But what was clear to us is that politicians by and large understand the difference between Libra and Bitcoin and are not threatened by regulated speculation on Bitcoin. Jay Powell’s Congressional testimony kicked off this string of political crypto events on July 10th, which marked the top of the market for July. In the subsequent seven days, BTC price marched down from $13k to $9.5k more or less unabated. This was the main contributor to BTC generating its first negative monthly performance since January. This price reaction was healthy and welcomed specifically in the context of the political backlash against Libra. Libra is good for Bitcoin, so to the extent there’s risk to Libra’s launch, that is negative for BTC on the margin. BTC price advanced aggressively into and after the announcement of Libra project details on June 18th. In our view, Libra was primarily responsible for taking BTC from $8700 to nearly $14000. While we believe the Libra project will ultimately come to fruition, a view we unpack in detail in our quarterly call, there is increased risk to Libra currently, and we could also just be wrong in our view that Libra will launch. So, a market backing out that bullish advance from $8.7k as Libra’s launch comes under intense regulatory scrutiny makes fundamental sense. Fundamentals driving price action is bullish crypto and bullish for Ikigai’s fundamentals-based investing strategies.

One factor that is unequivocally bullish is the Fed’s 25bps rate cut on the 31st. Bitcoin has never existed in a rate cutting cycle and every major central bank in the world is embarking on rate cuts and QE. If you follow central bankers’ words and actions closely, it is apparent that they are undergoing a race to see who can devalue their currency the fastest. This is deeply bullish for a non-sovereign, hardcapped supply, global, immutable, decentralized, digital store of value.

I sound like a broken record at this point but I’m not going to stop - we are living in a wacky time for global macro. Things are weird and getting weirder. Risks are pervasive. Hong Kong is a real risk. Europe is a real risk. The Fed Funds over the Interbank Offer rate is a real risk. Chinese bank collapse is a real risk. All of these risks have global knock-on effects. There are viable solutions to those situations, but those solutions require even more wacky central bank and government actions. Those are being enacted now.

Large-scale financial conditions have a long history of coming in waves and we’re seeing signs that this wave may be starting to come to an end. The 10+ year wave of monetary and fiscal policy irresponsibility from central banks and governments globally will produce a very different looking wave in the coming 10 and that setup is rife with risk. Ray Dalio wrote an exceptional post about it. Howard Marks, as he does, wrote a crystal clear memo about it. We are highly convicted that crypto will be at the foundational layer of this next wave.

At the current moment, we believe we have seen a shift in market structure and there is a chance we are seeing the first innings of a new regime - a topic we will dive into deeper below. There are significant risks to the downside at present - active portfolio management and strict adherence to risk management is required to generate attractive risk-adjusted returns.

While activity in July was a bit quiet given the summertime lull, we continue to field interest from new investors, evaluate new venture opportunities, build more tools to aid our investing strategies, and educate the public on this technology and asset class. We believe there’s never been a better time to be a crypto investor.

July Highlights

Chairman of the Fed Testifies to Congress About Crypto

President Trump Tweets About Crypto

Treasury Secretary Gives Formal Press Conference About Crypto

Congress Holds Two Day Hearing on Libra and Cryptocurrencies

SEC Grants Blockstack Approval for Reg A+ Token Offering

Bakkt Begins User Acceptance Testing for Bitcoin Exchange

Cash App Adds Bitcoin Deposits

Court Grants 90-Day Extension to Bitfinex/Tether in NYAG Case

Bloomberg Reports BitMEX Under CFTC Investigation

| Symbol | July | June | Q2-19 | Q1-19 | YTD | % ATH | % Cycle Low |

|---|---|---|---|---|---|---|---|

| BTC | -7% | 26% | 164% | 10% | 170% | -49% | 215% |

| ETH | -25% | 8% | 105% | 6% | 64% | -85% | 162% |

| XRP | -19% | -10% | 28% | -12% | -9% | -91% | 25% |

| BCH | -20% | -7% | 154% | -1% | 101% | -89% | 318% |

| EOS | -23% | -32% | 38% | 63% | 72% | -80% | 179% |

| BNB | -15% | -1% | 86% | 182% | 349% | 12% | 550% |

| XLM | -20% | -22% | -3% | -5% | -26% | -91% | 13% |

| LTC | -19% | 7% | 101% | 99% | 223% | -74% | 328% |

| TRX | -30% | -3% | 36% | 25% | 19% | -92% | 105% |

| Aggregate Mkt Cap | -11% | 15% | 117% | 14% | 120% | -67% | 173% |

| Aggr Alts Mkt Cap | -19% | 0% | 68% | 18% | 59% | -82% | 115% |

A Change in Season or Just a Temporary Weather Pattern?

If you’ve been following our work, you know we talk a lot about market structures and market regimes. We define market regimes as a combination of characteristics that lead to an overall direction, tone, risk and opportunity set of a given market. We think of market structures as temporary, mini regimes inside of a larger, overarching regime. A given market regime can have several, smaller market structures that come and go over the course of the broader market regime. Generally speaking in crypto, market regimes last for a handful of months and market structures last for a few weeks. So, its fair to think about regimes as seasons and structures as weather patterns. Over the last several weeks we believe we have seen a new market structure form. We identified this market structure forming from multiple angles using our proprietary tools – most notably in the volume and order book trends of major exchanges. It appears to us that multiple liquidity providers have pared-back their activities, leaving gaps in order books that has led to unnatural price action over the back part of July. These are dangerous grounds for trading. Stop losses can be triggered on a wick that never would have happened in a normal liquidity environment. With a shrunken order book, a smaller amount of capital is required for Risky Whales to initiate the chicanery we know they love. Why has this market structure shift occurred?

1. On July 19th, Bloomberg reported that the CFTC had been investigating BitMEX for several months, under suspicion that the unregistered exchange was allowing Americans to trade on it. This should come as little surprise to ecosystem participants – BitMEX is known for performing essentially zero KYC/Proof of Residency. All an American needs to trade on the exchange is a VPN. The BitMEX XBT Perpetual Swap is the most liquid Bitcoin instrument on earth – trading billions of dollars daily and having exceeded $10bn in volume on a single day earlier this year. It is undoubtedly one of, if not the, most important instrument for Bitcoin price discovery. In the days leading up to and after the Bloomberg article, BitMEX saw mass withdrawals, as shown below with July 19th noted.

The total amount of Bitcoin deposited at BitMEX peaked in March, began declining, and then saw an acceleration in decline several weeks before the Bloomberg article broke. Current balance stands at 165k BTC, down 35% from peak and down 20% in the last month alone. Is BitMEX’s run as king of crypto coming to an end?

2. Alameda Research is a quantitative crypto trading firm and currently the premier liquidity provider in the crypto space. They currently occupy two of the Top 10 positions on the BitMEX leaderboard for notional profitability.

This is demonstrable proof of their capabilities at providing liquidity. Earlier this year, Alameda began working on their own exchange, FTX, which launched in early March of this year - coincidentally (or not) the day that the BitMEX balance reached its all-time peak. FTX has its own token, FTT, similar to Binance’s BNB and Bitfinex’s LEO. Alameda owns a lot of FTT, and they are highly incentivized to drive adoption and volumes on FTX. There is good reason to believe they have pulled back their activities on BitMEX significantly to focus on their own exchange. Why would they help the competition?

3. Summertime is in full swing. Many crypto market participants are sitting on sizeable YTD gains. Things are good. Even quant strategies require a high degree of manual oversight in crypto. Did traders just turn the lights out and go to Mykonos for a month or two?

BitMEX/CFTC. Alameda. Summertime. These are the ingredients for the shift in market structure that we’ve witnessed over the last several weeks. The permanence, or lack thereof, of these factors is unknown. To what degree each ingredient is driving this new market structure is unknown. Will the CFTC investigation prove to be a non-event, and BitMEX activity will pick back up? Will another liquidity provider of equal prowess pick up where Alameda left off? Will everyone get back in front of the screens after Labor Day and we’ll see liquidity come roaring back to life? We don’t know the answers to these questions yet. We think these are just temporary choppy weather patterns within an overall bullish season. But there’s a chance the season may be changing. We’re watching carefully.

Ikigai’s Investment in Digital Assets Data

Here at Ikigai we are large consumers of crypto data. Ingesting, synthesizing, analyzing and drawing investable conclusions from the host of quantitative and qualitative data generated by the crypto space on a daily basis is at the core of what we do. The quantitative data can broadly be bucketed into on-exchange and on-chain data (although there are other categories, like sentiment). About a year ago we began building the infrastructure to ingest and synthesize this data, and we immediately began running into problems. I won’t go into too much detail around those problems because they have been well-documented in the ecosystem – poor quality exchange API’s; historical data with holes in it; broken websockets; difficulty running nodes and extracting data. And it was expensive – we immediately found ourselves paying thousands a month in AWS bills, not to mention the manpower to deal with it all. In the meantime, we were also evaluating many third-party data providers. So, by early 2019, we had a firsthand, comprehensive understanding of the crypto data landscape, it’s challenges, and its players. We were acutely aware of how hard it was to handle crypto data really well in-house. Some of the data service providers were good, others were not so good. None were a one-stop shop.

In February we began having discussions with the Alfred brothers - Ryan and Mike, and their CTO Kurt Fenstermacher, about their soon-to-be-launched platform Digital Assets Data, or DAD. From the beginning, we were incredibly impressed with the team. Not only were their backgrounds stellar, but their attitude, approach, responsiveness and character were exactly what you would want to see in a partner. DAD was pitched to us as a “crypto data chassis” and took a fundamentally different approach than anything else we’d seen from third-party crypto data providers. DAD aimed to entirely remove the need to store data and analysis ourselves. Instead, they would ingest, synthesize and store all of it, and make it available to customers in a detailed and easy to use callable Python library. Their pricing structure relative to our AWS bill + manhours was compelling, and they came with a lot in-house expertise to help with product development and rollout.

In May we came on as a customer. We worked closely with many members of the DAD team and stayed in constant contact with Ryan and Mike. The product was relatively bare bones when we joined in early May, which we were expecting. Ryan and Mike told us from the beginning that a bet on DAD was a bet not just on what they had, but what was coming, the quality of those products, and how quickly they would ship. We have been impressed with their pace of rollout and their ability to set delivery dates and stick to them. The product is meaningfully more robust today than it was May 1st, June 1st and July 1st. DAD is currently storing more than 15 terabytes of crypto data. We expect the product to be meaningfully more robust by year-end, Q1-20, and so on. In June, Ryan and Mike told us they were doing a follow-on equity raise to their $3.2mm seed raise, led by Silver Lake co-founder Glenn Hutchins, and invited us to invest.

We have a simple but unique hurdle for considering venture investments in crypto – the investment needs to beat the expected returns of BTC over the holding period on a risk-adjusted basis. I’m not sure how many crypto funds think about it like that, but our mandate allows us to deploy 100% of our capital into liquid crypto if we don’t find anything compelling on the venture side – that flexibility in strategy was important to us when we formed Ikigai. We also want to find investments where we have expertise. We felt we knew DAD’s market as well as anyone, we believed their value proposition, and we experienced the product for months firsthand. To be clear, our base case is not that our DAD investment outperforms BTC on an absolute basis over the investment period. If BTC does a 6 bagger over the next three years, we are not expecting a 10x on DAD. Instead, we see the level of certainty of a path to an attractive rate of return compelling. We believe in DAD’s value proposition and its ability to scale to a massive addressable market. We believe in the team to deliver that.

Market Update - Liquid Crypto Asset Investing

After its fourth best quarter in the last thirty, BTC price pulled back 7% in July. That relatively mild price decline belies a large trading range – at different points in July, BTC was both up more than 20% and down more than 15%. As discussed above, that price action came in chunky moves. On the morning of July 9th, we witnessed someone sell 7,500 BTC at market on Binance – a tremendously strange event – only to see price rocket $1,000 higher in the 24 hours after the sell wall was cleared, before collapsing $2,000 in the following 24 hours. Choppy indeed.

Alts faired worse than BTC in July – with the Aggregate Alt Market Cap declining 19% on the month. That puts Alts up 59% YTD vs BTC +170%. LINK, BNB, LTC and THETA are the only major Alts to outperform BTC YTD. We would argue only BNB has outperformed BTC on a risk-adjusted basis. This underperformance is a healthy and welcomed response, because it is rational. The value proposition of most Alts has been inferior to BTC, and disappointingly so. That said, we believe this is a moment in time. The Alt space is iterating at a breakneck pace. We believe there will be many crypto assets that gain mass adoption and create tremendous value. Smart contracts will be ubiquitous and unlikely to be built on the Bitcoin network. It is our base case that at least a handful of Alts will outperform BTC on an absolute basis during this current bull cycle. We think it is likely that a smaller handful of names may outperform BTC on a risk-adjusted basis. It is our job to find those names. There may be periods of time, fondly referred to as “Alt Season”, where Alts broadly present compelling risk-adjusted return opportunities relative to BTC. It is our job to identify those periods. These seasons may come after an instance of capitulative Alt selling, which we believe may have occurred on July 16th. We believe a period of broad Alt outperformance may be around the corner, but it’s too early to know with conviction. If Alts broadly, or an individual Alt specifically, don’t present a compelling risk-adjusted return opportunity, it is our job to avoid that exposure.

Currently BTC is in the midst of a pullback. As previously mentioned, the nature of this price action has made the recent period difficult to have a firm grasp on. We currently believe this pullback is transitory but are not currently highly convicted that we won’t see a lower low before seeing a higher high. From a Wyckoff/Risky Whale perspective (they are one in the same to us), it is unclear whether we are still in a distribution phase or halfway through a re-accumulation phase. When the answer becomes clear, we believe we’ll see it and will act on it.

We have had a collapse after a parabolic advance. That is to be expected.

The depth of that pullback after a parabolic advance is often best determined with Fibonacci retracement. We broke both the 23 and 38 Fibs, which puts the 50 in play at ~$8500. Many market participants are calling for this level. That makes us think we will either go meaningfully lower or never get that low. The herd is rarely correct. The outcome remains to be seen.

By many of our proprietary measures, on-chain metrics look bad. In July they mostly got worse. Market prices appear to be too higher relative to on-chain activity. We have discussed this relationship at length, so you know we believe there is good reason for this to be occurring - an increasing price that is outpacing an increase in network activity. This is a publicly available example of this.

A price that stays in this current very broad range – say from $7k to $14k over the next 3-6 months, may allow on-chain metrics to “catch up” to market prices, a period we call Re-Accumulation. We believe it is possible that’s where we are now. If this chart proves correct, we are setting the stage for fireworks in 2020.

After a breathtaking ascent YTD, on-exchange volume remained significantly elevated in the first part of July, only to collapse lower in the back part of the month – further evidence of the previously mentioned market structure shift. The trailing 7-day avg volume at the end of July was a 60% lower than at the end of June, albeit only pulling back to May levels. We think we know why volumes declined so much in the back part of July, and we think those reasons are transitory – weather not seasons. But we’re watching closely. BitMEX volumes in turquoise.

BTC monthly chart shown below. Note that Coinbase volume actually increased M/M, which speaks to our point about BitMEX activity declines in late July in the context of the above chart. Also note that at the beginning of the last bull market we had two consecutive months of declining prices, with a pull back of ~37% peak to trough. The current pullback is 36% peak to trough. Note that during the raging bull market of 2017, we did not pull back two consecutive months.

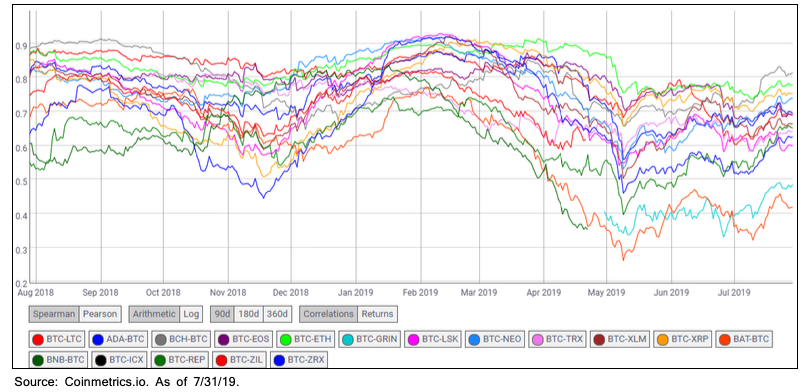

Cross-coin correlation declined in the first part of July and then increased into the back part as BTC price declined. This range is healthy.

Hashrate made new highs in July. We are witnessing an increasingly more secure network. This is bullish.

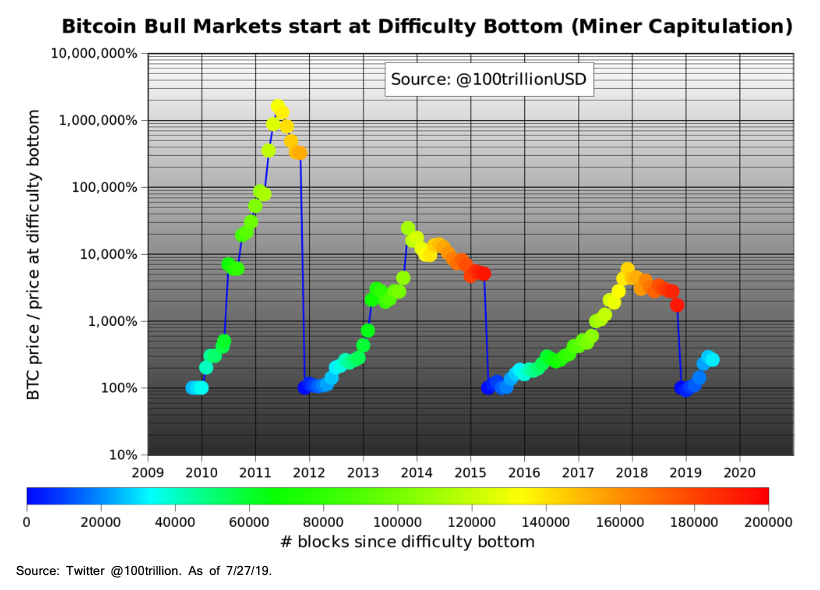

Another way to think about hashrate is through the lens of difficulty. Difficulty adjusts downwards when hashrate declines for a significant amount of time. This is a beautiful feature of the Bitcoin network. Hashrate tends to decline when price declines by a significant amount for a significant length of time. The below chart is a ratio of current BTC price to BTC price at cyclical difficulty bottoms, with a heat map of monthly points since that cyclical difficulty bottom. This is convincingly bullish about where we are in the cycle.

Stock-to-flow (S2F) is the amount of supply divided by the amount produced annually. It is a measure of abundance. Stores of value have high S2F. The below chart shows various stores of value – gold, diamonds, BTC, etc. The y-axis is market cap of the given store of value and the x-axis is the S2F of each. For Bitcoin, a heatmap of points is shown based on months until halving, where the S2F steps up systematically through a reduction in block rewards. The line shown for BTC in the future is based on a best fit with a 0.99 R2. Should the world decide BTC is fit to be a money, this is captivatingly bullish – there is simply not enough BTC to go around without massive price increase.

Trailing 24hr BTC realized volatility (yellow) vs BTC (orange). After squeezing from November to April, we entered a period of increased volatility through to the cycle highs in late June. Volatility collapsed in July and is now reaching the zone of cycle lows (blue circle). It could leak lower for a while longer, but when it breaks out, expect a large move in price one direction or the other.

Closing Remarks

The crypto market pulled back a bit in July under a white-hot political spotlight. The fifth largest company in the United States, and the largest social media company in the world, has entered the crypto ecosystem in a major way - with its own method of exchange meant to bring the concept of digital value accrual to 2.4bn monthly active users. Given Facebook’s disregard for data privacy and the bipartisan popularity of disliking the company, politicians’ backlash against Libra comes as no surprise. But take a step back and look at the forest through the trees – crypto is moving front and center to the global stage. This is no tulip. This is the most important technological innovation since the internet the first time around.

Meanwhile, the global macro backdrop continues to paint a wildly bullish picture for Bitcoin while Bitcoin ecosystem developments continue at an impressive pace. The New York Stock Exchange will trade it. Fidelity will custody it. Microsoft will build on it. Whole Foods will accept it. And every major central bank on the planet will race to see who can devalue their currency the fastest. That’s happening.

“I’ll do my best to find my dreams and goals.”

Travis Kling

Founder & Chief Investment Officer

Ikigai Asset Management

Invest

Ikigai is currently fielding interest from new investors. Contact us to see if you qualify.

P.S.

Included below is an incomplete list of memorable tweets from the last month. Twitter is not investment advice and my views could easily be wrong. That being said, like it or not, Twitter matters for crypto. I have no interest in being a talking head for a living and babbling about on Twitter is a long way away from being a good steward of investor capital. However, this is a community with open-source software in its DNA, and participants want to crowd-source the truth. We believe we have built a team and a process that will produce these truths more quickly and more clearly than our competitors. We are shepherds of this technology. Answers to fundamental questions about this asset class are not currently clear, so having a public platform to share your views with the community is important. After all, you’re helping shape the future :)

1. Ikigai Asset Management is the trade name for a collection of advisory and consulting businesses operated by Travis Kling, Timothy Lewis, Anthony Emtman, and their team.

The information contained or attached herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. This presentation may contain forward-looking statements that are within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements are based on management’s beliefs, as well as assumptions made by, and information currently available to, management. Although management believes that the expectations reflected in these forward-looking statements are reasonable, it can give no assurance that these expectations will prove to be correct. This email is for informational purposes only and does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product, service of Ikigai as well as any Ikigai fund, whether an existing or contemplated fund, for which an offer can be made only by such fund’s Confidential Private Placement Memorandum and in compliance with applicable law. Past performance is not indicative nor a guarantee of future returns. Please consult your own independent advisors. All information is intended only for the named recipient(s) above and is covered by the Electronic Communications Privacy Act 18 U.S.C. Section 2510-2521. This email is confidential and may contain information that is privileged or exempt from disclosure under applicable law. If you have received this message in error please immediately notify the sender by return email and delete this email message from your computer. Copyright 2019 Ikigai Asset Management, LLC. All Rights Reserved.

NOT INVESTMENT ADVICE; FOR INFORMATION ONLY

PAST PERFORMANCE IS NOT A GUARANTEE OF FUTURE RESULTS