February 2019 - Market Update

/Monthly Update || February 2019

“To achieve superior investment results, your insight into value has to be superior. Thus you must learn things others don’t, see things differently or do a better job of analyzing them — ideally, all three.”

OPENING REMARKS

Greetings from inside Ikigai Asset Management headquarters in Marina Del Rey, CA. We welcome the opportunity to bring to you our fifth Monthly Update and hope these are helpful in better understanding some of what we’re doing and what we’re seeing. We have the privilege of deploying capital on behalf of our investors into a new technology and asset class that we believe will fundamentally change the world and create trillions of dollars of value in the process. We believe we are obligated to be shepherds of this technology – to help the world better understand the powerful potential of DLT and crypto assets, and to fund and be an ambassador for DLT projects that will change our lives forever.

To that end, we continue too closely monitor the crypto market to help us understand where we are in the cycle. We are creating groundbreaking new Fundamental Valuation methodologies to triangulate when and where a bottom might occur for this market, the nature of that bottom, and what the subsequent beginnings of the next bull market might look like. We believe there are extremely few, if any, market participants that are seeing this market as clearly as we are currently. Our Four Foundations generate a couple dozen signals in aggregate, both quantitative and qualitative. We take the preponderance of evidence from those signals across the Four Foundations and make investment decisions accordingly. Those Four Foundations are the product of a couple thousand hours of research and analysis, and the signals they generate continue to be more accurately dialed in, as our process is consistently and endlessly improved upon.

In the month of January we traveled to San Francisco, Miami, Utah, Hong Kong, Japan and South Korea- meeting with dozens of founders, developers, exchanges, investors and other noteworthy ecosystem participants. The “crypto winter” is being felt by everyone everywhere. Many topics are front burner for the community at the moment- STO’s, stablecoins, regulation, governance, scaling solutions, new projects and infrastructure, price action and traditional asset class correlation, to name a few.

The current view from outside the industry looking in is in many cases some mix of mild interest and confusion. Many investors without current exposure to the space want to learn more, but price declines coupled with hacks, scams and regulatory uncertainty give them little sense of urgency in getting up to speed to deploy capital in the next couple months. Other investors have dug in more deeply, seeing the broad potential of DLT, but are having trouble identifying the type of exposure to the space they desire. Still other groups of “no coiners” are feeling highly vindicated in their stance to remain entirely out of the mania of 2017 and the subsequent crash of 2018- this group of investors remains skeptical of the long-term value proposition of DLT and crypto assets and have circled up around fallacies like “blockchain not Bitcoin”.

From the inside looking out, there is a view that much of the groundwork is being laid right now to serve as the foundation for the next bull run. Human and financial capital continue pouring into the space, albeit at a slower, more sustainable pace and in a more cautious, discerning manner- this is a good thing. Token structures, token distributions, fundraising strategies, governance, use cases and infrastructure are iterating quickly. New generations of technology are introduced quarterly. All of this is moving at a breakneck pace. There is a lack of clarity at the current juncture as to the eventual form these iterations will take. There is a “primordial soup” characteristic to the current market environment. We can see many exciting pieces floating around in this market, components that we believe have the characteristics to be part of projects that change the world forever. But a lightning bolt hasn’t quite struck yet to create the amino acids of compelling long-term value accrual. Nevertheless, it is clear to us that the pieces are in place for this to occur. Our hardworking, talented team at Ikigai is deeply entrenched in the ingestion, synthesis and analysis of all the new information produced by this primordial soup. It the basis upon which we make investment decisions every day.

JANUARY HIGHLIGHTS

Highly Anticipated Privacy Tokens Grin and Beam Launch

Colorado Digital Token Act Creates Exemptions From Certain State Laws

VanEck ETF Application Withdrawn And Refiled

ETH Upgrade Constantinople Delayed After Security Bug Found

Coinstar To Add Bitcoin Purchases At Kiosks

UK Securities Regulator Rejects SEC Stance On Utility Tokens As Securities

Leaked Pictures Of New Samsung Galaxy Show Built-in Blockchain Wallet

BitTorrent ICO Raises $7.2mm in 15 Minutes

THE FED BLINKS

From our vantage point, spending the majority of our waking moments researching, analyzing and investing in DLT in crypto assets, sometimes its easy to lose sight of the forest through the trees. With BTC -85% from its highs 400+ days ago and the ecosystem in the midst of a brutal bear market, it is possible to lose sight of the value proposition of DLT and crypto assets. Why does decentralization matter? Why does the world really need any of this technology? What problems that need solving can be solved?

From time to time, events happen that remind us why we believe there is an inevitability to the mass adoption of this technology and asset class. January 30th was one of those days. The Fed held its regularly scheduled FOMC meeting with a statement and press conference and the stance revealed by Jay Powell and the Fed was a capitulatory leap towards dovishness relative to only 6 weeks prior.

On the path to future rate tightening, the Fed removed any reference to a gradual increase in rate hikes and replaced it with language around patience, acknowledgement of downside risks, tightening financial conditions and a lack of inflationary signals. In this meeting, the Fed moved decisively towards being “on hold” and even opened up the door for possible future rate cuts. Nothing short of a complete about-face from mid-December.

On the balance sheet runoff, the Fed backed away from that as well, stating:

“The Committee is prepared to adjust any of the details for completing balance sheet normalization in light of economic and financial developments. Moreover, the Committee would be prepared to use its full range of tools, including altering the size and composition of its balance sheet, if future economic conditions were to warrant a more accommodative monetary policy than can be achieved solely by reducing the federal funds rate".

While risk assets had rallied meaningfully in the weeks leading up to this meeting based on more dovish stances from the ECB, PBoC and BoJ and on the assumption that the Fed was going to also move towards a more dovish stance, the Fed utterly succumbed even more than expected to the whims of the market and Trump’s Twitter prodding.

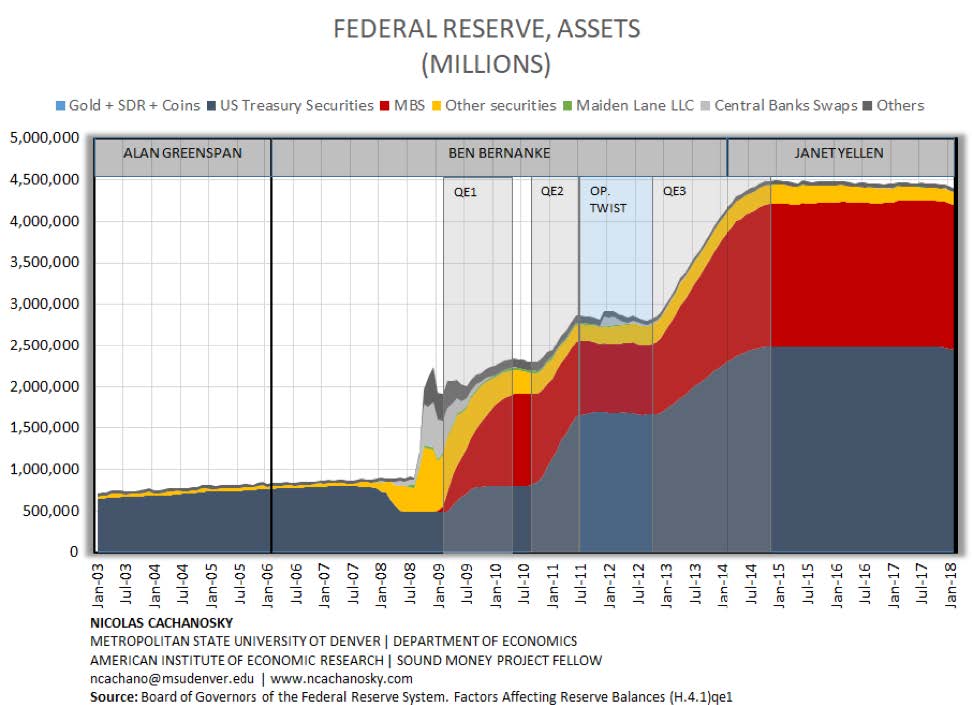

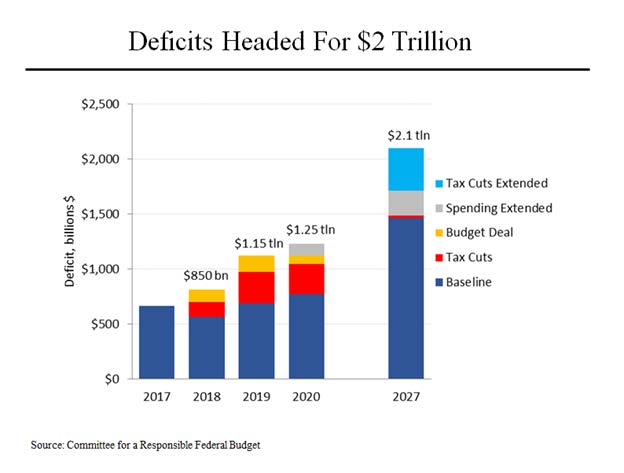

Subsequent to the FOMC meeting, risk assets rallied, gold rallied, VIX collapsed, USD dropped and interest rate curves steepened aggressively. The mantra of “don’t fight the Fed” again made the rounds as it has so many times in the last decade. As of January 31st, the market is now pricing in no more rate hikes in 2019 and rate cuts beginning 2020. Talk about a policy shift. This event, the Fed’s about-face, is deeply bullish crypto but in a scary sort of way. We are undergoing the largest monetary and fiscal policy experiment in human history- Quantitative Easing while simultaneously running massive budget deficits on top of an increasingly untenable debt level.

Source: Committee For A Responsible Federal Budget. 2018.

It would be naïve to think this experiment is going to end without significant market stress. A bet on BTC (or perhaps some other monetary cryptocurrency) is opting out of this experiment. Whether its 1% or 5% or 25% of a portfolio, a bet on crypto is taking a stance that there’s a chance this experiment could go very wrong, and portfolio protection from that downside scenario is warranted. If you were going to write the script for a non-sovereign, hardcapped supply, digital form of money to gain mass adoption, this is how you would write it- an increasingly erratic president yelling at an irresponsible central bank to act even more irresponsibly with its monetary policy. The more irresponsibly central banks and governments act with their monetary and fiscal policies, the more compelling the case for crypto. We believe that case for crypto became meaningfully more compelling in January in light of the Fed’s actions.

Money printing is a drug. Risk assets have been on that drug for 10 years. Risk assets are addicted to that drug. The Fed is the parent of a kid with a drug problem. The kid needs tough love to get off the drug. The parent tried to lock the kid in his room to get him off the drug. The kid began going through withdrawals and throwing a tantrum. The parent didn't have the willpower to keep him in his room to get him off the drug. The kid is going back outside to "hang out with his friends". This is unlikely to end well.

THE CURRENT STATE OF CRYPTO: WHAT HAVE WE LEARNED?

We have put in thousands of hours of aggregate research and analysis to build out our Four Foundations and continue to do so on an ongoing basis as we strive for continuous improvement. As a result of that past and ongoing work, we believe we have about as good of a look as anyone into what is happening with this space and what we might expect to happen going forward. Our views change rapidly, and we reserve the right to alter our stance at a moment’s notice if new information becomes available. But the following is a list of insights we have gleaned that we deem especially important and more probable than not to be true. Some of these may be evident to you, some you may disagree with and others might not make sense to you. They are meant to be bitesized appetizers to jump off into further contemplation and research. As always, we are available to discuss in more detail. If you’re interested in learning more, just reach out.

Money is the killer app for DLT right now. The value proposition for BTC relative to its status quo (i.e., gold) is much more clearly understood than any other crypto asset’s value proposition is relative to its unique status quo.

The Velocity Problem is real. The Working Capital Problem. Chuck E. Cheese problem. All else being equal, the faster a token spins through an ecosystem, the lower the price of that token needs to be to satisfy the economic demands of that ecosystem. Money as a use case does not have this problem.

The Deflation Problem is real. If a rent-seeking middleman is charging $100 for $10 worth of services, a DLT may very well be able to provide that service for $2. But that’s not so much a great investment proposition in the DLT as it is an awesome deal for the consumer. Money as a use case does not have this problem.

The value created by the technology and the value accrued by the crypto asset are two different things. The bridge between those is token structure. For many types of crypto assets, we have not discovered a token structure that allows for the value created by the technology to be accrued in the token in the long term.

Stablecoins are going to be systemically important for years, if not forever. BTC works so well as a SoV that it doesn’t work very well as a method of exchange and likely won’t for many years. Stablecoins can be Venmo to the world.

The market is not accurately ascribing fundamental value to projects. ETC was 51% attacked and has a current market cap >$400mm. NEO went 4 hours in late January without generating a block and has a current market cap of >$450mm. There is >$350mm aggregate market cap in actual scams.

Most things don’t need a blockchain. We will see continued moves towards application layer solutions that capture value.

The Fat Protocol Thesis as it was applied to consensus protocols was a fallacy. Value accrual on a large scale will require network effect for most crypto assets, which will require “last mile” access to users. Underlying consensus protocol value may trend towards the marginal value of the utility provided.

DAOs will likely be a big part of our future. This will take decades to play out, but the first pieces are beginning to fall in place already. Enabling the trust revolution.

Lightning Network is under-discussed and over-achieving. From zero to >2,700 active channel nodes in a year. $2mm of current capacity.

“DeFi” is 18-24 months away but the stack could end up being compelling. Wyre + Dai + Compound + Balance.io gives a glimpse into what could be possible.

Prediction markets may be the most compelling use case after money. The Oracle Problem refers to the difficulty in accurately, trustlessly writing real-world things to a blockchain. Prediction markets could solve that.

Layer 2 scaling makes sense and the market is coming around to that. State channels on ETH- Funfair; Raiden; Spankchain Lightning Network on BTC.

Privacy is coming to most/all chains. Mimblewimble; Starks; Snarks; Ring signatures; but current demand is unclear.

ETH 2.0 is a long way away and the path to execution is highly uncertain. Five part, multiyear process. Several parts have no clear path to a solution.

Money is pouring into infrastructure but its not currently sufficient. UX is still clunky. Untrustworthy exchanges still have volume.

Digital wallets will be ubiquitous. WeChat already. Facebook Messenger coming. Venmo has the 4th largest number of users of any U.S. bank after Wells Fargo, BofA and Chase.

MARKET UPDATE – LIQUID DIGITAL ASSET INVESTING

Crypto prices declined in January, with the notable of exception of TRX. Under the surface, the month exhibited broadly weak demand and an inability to muster even meager attempts at sustainably higher prices. BTC price has now declined 6 consecutive months, the longest streak in history. At time of writing, a retest of the mid-December lows of ~$3150 appears likely to occur in February, and we believe it is likely only a matter of time before that support level breaks and we make new lows.

Of note, BitTorrent completed an ICO of its new token BTT that raised $7.2mm in 15minutes on Binance at a price of $0.00012. Tron, which owns BitTorrent, also plans to airdrop 10.9bn BTT to TRX holders on Feb 11th. While details have not been released, BitTorrent plans to build out a streaming platform on Tron’s network that will launch sometime in 2019. This hype around BTT has allowed TRX to rally >100% from late- November lows- massively outperforming BTC over this time. Importantly, there appears to be little technological substance underpinning Tron’s platform. The former Chief Strategy Officer of BitTorrent stated in January that TRX is woefully inadequate for running BitTorrent at this time and most likely won’t be used at all to power BitTorrent. TRX founder Justin Sun has been all marketing and no substance from the beginning of the TRX project, which plagiarized significant portions of its whitepaper. TRX is based in South Korea, the hype capital of the crypto universe. Upon initial trading on Binance, BTT traded as high as 5x the ICO price and has currently settled in at ~4x the ICO price. We believe the crypto market’s willingness to drive prices up to these levels on such little substance is one signal that the overall market has not yet bottomed.

Even with the 35% increase in TRX in January, the Bottom 99 still declined 11%, led by ETH, XLM and BCH. Bottom 99 is currently 15% above the mid-December lows, but there is very little bid for any of these names as volumes continue to decline significantly. Selling just $0.5mm of many names would push the price down >10%. We believe Bottom 99 will make new lows in the coming months.

Source: Coinmarketcap. As of 1/31/19.

Details around ETH’s scaling solution, dubbed “ETH 2.0”, continue to emerge, and the market is processing how enormously difficult and lengthy this upgrade process for ETH will be. We believe the $80 mid-December low for ETH will likely be revisited and broken in the coming months. We implement several sentiment analysis tools, one simple one is BTC tweet counts. On that metric, we appear to be nearing peak apathy by historical measures.

Source: Bitinfocharts.com. As of 1/31/19.

Cross Coin Correlation, one of our major signals for determining market environments, increased in January and remains near all-time highs. It is difficult to make disparate bets in the current market environment as essentially everything is one big directional trade right now. We believe this is a sign the market has not yet bottomed.

Source: Coinmetrics.io. As of 1/31/19.

Volumes are declining. Aggregate global BTC volume shown below (17 largest exchanges included), declined ~40% in January as measured by the 7 day moving average (shown in light blue). Increased correlation in conjunction with declining volumes in the context of many of our other proprietary signals, tells us this market is likely squeezing in advance of further price declines.

Source: TradingView. As of 1/31/19.

We have developed new proprietary valuation methodologies based on derivations of on-chain metrics and wallet forensics that we believe give us best-in-class accuracy in understanding crypto market cycles and characterizing the bottoming process. Some of these methodologies have given us fascinating insights into the nature of historical and current network activity and its relationship to network value. The preponderance of evidence across these metrics and many others points to valuations that are still elevated but are generally trending in the direction of finding a bottom. While we are not going to share these valuation methodologies here given what we believe to be their alphagenerative characteristics, feel free to reach out directly if you’d like to learn more.

CLOSING REMARKS

The crypto market started 2019 with a continuation of the negative price action seen in late 2018. The bear market is being felt everywhere. Outside interest is fading. Volatility seekers have turned back to traditional asset classes, which are having their own fireworks at the moment. Crypto currently has little to show for itself by way of adoption and usage in the everyday world. But under the surface, a tremendous amount is happening. The ecosystem’s understanding of value accrual is maturing. Technology and business models are iterating. Infrastructure buildout and regulatory clarity are progressing. Pieces are coming together that will soon give rise to a new era for crypto.

Our conviction remains unwavering. We believe we are nearing a period of incredible opportunity for generating risk-adjusted returns that will far exceed any other asset class. We believe we have the frameworks, processes and tools in place to understand what that market structure will look like and how to best capitalize on those opportunities. There is an inevitability to the direction and distance this technology and asset class will go. The world isn’t going to wake up tomorrow and decide not to use this technology, any more than the world would wake up and decide autonomous cars aren’t compelling, or augmented reality isn’t fascinating. While we’re not precisely sure about the path of the train tracks or the speed of the locomotive, the crypto train has left the station and is moving down the track towards a multi-trillion dollar valuation. It isn’t stopping.

“A smart man has big ears.”

— Ancient Japanese Proverb

Travis Kling

Founder & Chief Investment Officer

Ikigai Asset Management

P.S.

Included below is an incomplete list of memorable tweets from the last month. Twitter is not investment advice and my views could easily be wrong. That being said, like it or not, Twitter matters for crypto. I have no interest in being a talking head for a living and babbling about on Twitter is a long way away from being a good steward of investor capital. However, this is a community with open-source software in its DNA, and participants want to crowd-source the truth. We believe we have built a team and a process that will produce these truths more quickly and more clearly than our competitors. We are shepherds of this technology. Answers to fundamental questions about this asset class are not currently clear, so having a public platform to share your views with the community is important. After all, you’re helping shape the future :)

1. Ikigai Asset Management is the trade name for a collection of advisory and consulting businesses operated by Travis Kling, Timothy Lewis, Anthony Emtman, and their team.

The information contained or attached herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. This presentation may contain forward-looking statements that are within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements are based on management’s beliefs, as well as assumptions made by, and information currently available to, management. Although management believes that the expectations reflected in these forward-looking statements are reasonable, it can give no assurance that these expectations will prove to be correct. This email is for informational purposes only and does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product, service of Ikigai as well as any Ikigai fund, whether an existing or contemplated fund, for which an offer can be made only by such fund’s Confidential Private Placement Memorandum and in compliance with applicable law. Past performance is not indicative nor a guarantee of future returns. Please consult your own independent advisors. All information is intended only for the named recipient(s) above and is covered by the Electronic Communications Privacy Act 18 U.S.C. Section 2510-2521. This email is confidential and may contain information that is privileged or exempt from disclosure under applicable law. If you have received this message in error please immediately notify the sender by return email and delete this email message from your computer. Copyright 2019 Ikigai Asset Management, LLC. All Rights Reserved.

CONFIDENTIAL – NOT FOR FURTHER DISTRIBUTION

NOT INVESTMENT ADVICE; FOR INFORMATION ONLY

PAST PERFORMANCE IS NOT A GUARANTEE OF FUTURE RESULTS