June 2024 - Monthly Market Update

/Monthly Update || June 2024

“Investment success requires sticking with positions made uncomfortable by their variance with popular opinion.”

Opening Remarks

Greetings from Ikigai Asset Management¹. We welcome the opportunity to bring to you our sixty-ninth Monthly Update and hope these are helpful in better understanding some of what we’re doing and what we’re seeing. We have the privilege of deploying capital on behalf of our investors into a new technology and asset class that has tremendous potential to make the world a better place and create trillions of dollars of value in the process.

We believe we are obligated to be shepherds of this technology – to do our part to push crypto towards fulfilling its potential. We strive to be an objective, reasonable, well-intentioned voice of truth amongst a chorus of biased, fallacious, pernicious opportunists. It’s an honor that we take seriously.

To that end, wooo weee! What. A. Month. It is not an exaggeration to state that May 2024 was the most significantly positive month in crypto history from a regulatory/political perspective. And like many things in crypto, it evolved extremely rapidly and caught virtually everyone by complete surprise. We will dive into the details below, but suffice it to say this was a massive shift for the crypto markets relative to one month ago. It is a big deal.

A month ago here, we were talking about the struggles in macro as the market adjusted to less cuts and the potential for no rate cuts at all, coupled with the struggles in crypto as we moved into summer with heavy bags and little discernable narratives for Alts. Fast forward a month and both of those setups have meaningfully changed, for the better.

Macro fears around rate cuts were allayed as Powell stepped up to the mike on May 1st and delivered a decidedly dovish message. The Fed would begin slowing the pace of tapering in June. He put fears of an impending rate hike to bed. And when asked about stagflation he said “I don’t see the stag and I don’t see the flation”, which is a pretty epic line. It was A-game Powell and the markets rewarded it. In the days and weeks that followed, we got light jobs data, light inflation data and a great earnings report for our Lord and Savior Jensen Huang at Nvidia. Put it all together and Q’s were +6% in May and the DXY was -2%. Going forward, macro is still hinging on economic data and FedSpeak, but the risks have diminished in the near-term.

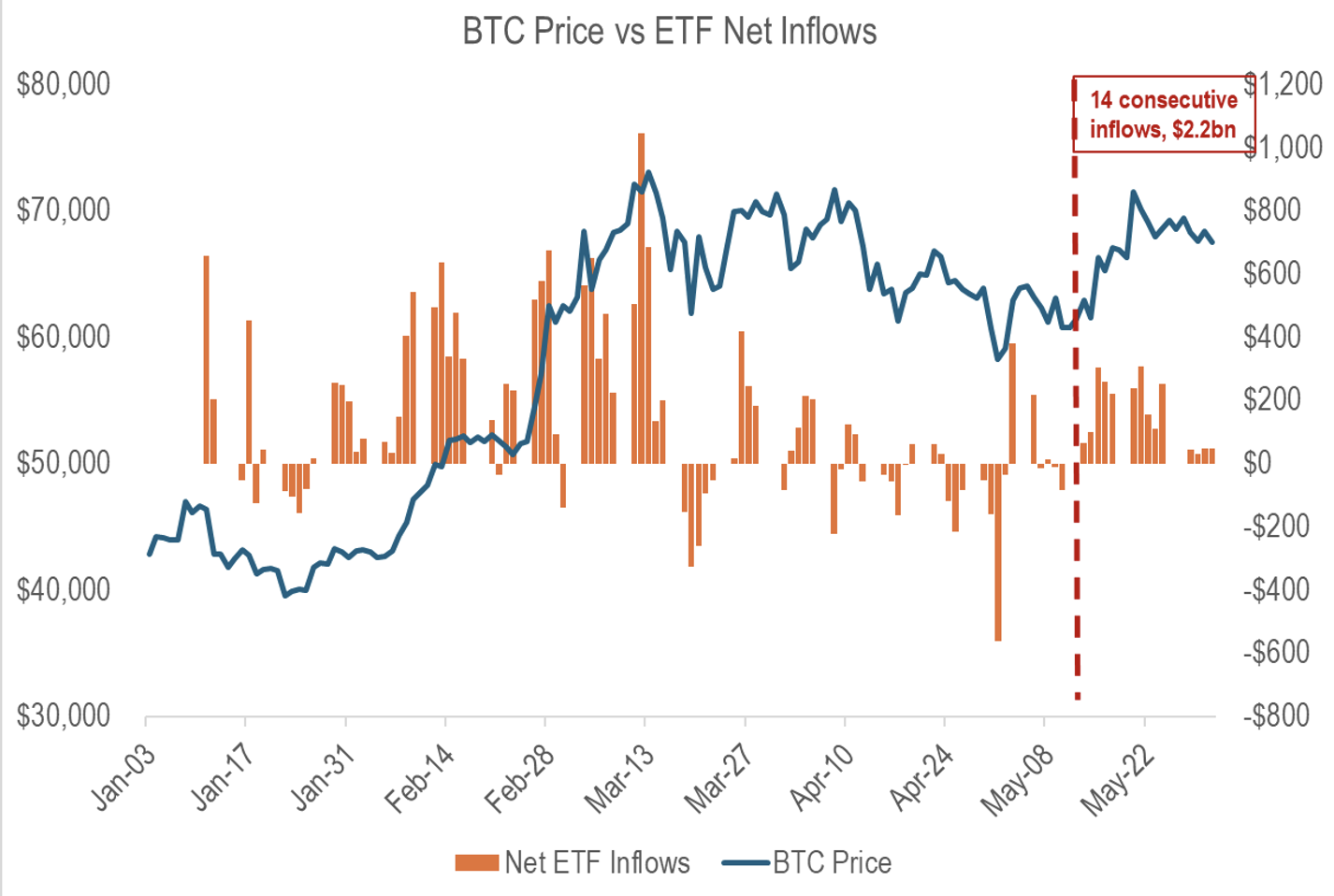

When it comes to crypto, BTC ETF inflows turned around and BTC price turned right around with it. You can’t help but think that inflow pickup was related to the macro shift mentioned above. It all lines up pretty well.

Source: farside.co.uk. As of 5/31/24.

Additionally, you had 13F filings on the BTC ETFs for the first time. We talked last month about how important these filings were going to be. Overall they were enlightening and generally positive. Here are some links to more information on the 13F filings. Millenium owns $2bn in total across many ETFs, Susquehanna owns >$1bn in total across many ETFs. There are a few other hedge funds of that caliber and ilk that own less but still significant amounts. It brings up an interesting question about the nature of these holdings for very large hedge funds that have highly sophisticated strategies, both HFT and otherwise. The hedge fund holdings point to an arb that likely exists and is being exploited. That said, if you’re Millennium it’s pretty unlikely you hold $2bn of BTC ETFs for strictly “arb”, so there is likely other stuff going on regarding the nature of the ETF holdings in these sophisticated hedge funds. Many of the hedge funds with the largest ETF holdings run multifactor, cross-asset, risk parity types of strategies. Simplistically, this would be the type of strategy that might long Bitcoin and short the US10Y because the models say that Bitcoin is “cheap” to the 10yr. These types of strategies manage hundreds of billions, if not trillions. It’s worth noting that these types of strategies will sell aggressively and indiscriminately when the model says to sell, so it’s worth keeping an eye out. But you also had the 9th largest pension in the US, the state of Wisconsin, buy $99mm of the ETF. And a bunch of reasonably sized RIAs along with it. So overall I’d say the 13Fs were good. If the state of Wisconsin could bring about a dozen of its friends along with it and crank that size up, we could get some real fireworks later this year.

Finally, and as initially alluded to, you had the Democratic party’s stance on crypto effectively unravel over a period of a few weeks. You had Trump essentially forcing the Democrats to pivot by publicly siding with crypto. You had spot ETH ETFs approved. You have an actual shot at real crypto legislation being passed as law. It is an incredible, almost unimaginable turn of luck for crypto that has significant ramifications.

Just when it seems like things are looking dicey!

May Highlights

Congress Votes to Repeal SEC’s SAB 121, Garnering 21 out of 213 Democrat Votes

Trump Says He’s Supportive of Crypto, Says If You Like Crypto, You Better Vote for Him; Allows Donations to Be Made in Crypto; Makes Additional Strongly Supportive Statements; Pledges to Pardon Ross Ulbricht If Elected

Biden White House Issues Press Release Saying He Will Veto SAB 121 If It Passes Both Houses

Senate Votes to Repeal SAB 121, Garnering 12 out of 46 Democrat Votes

Biden Vetoes SAB 121 Repeal

FDIC Chair, Leader in Operation Chokepoint 2.0, Steps Down

Out of Nowhere, Domain Experts Begin Circulating Rumors ETH ETFs Will Be Approved on May 23rd, After Assigning Little Chance of Approval

Three Republicans and Two Democrats Write Letter to Gensler Urging Approval of ETH ETFs

SEC Requests Accelerated Updates to 19b-4 Filings for ETH ETFs, Staking Removed

SEC Approves 19b-4 Applications for Nine ETH ETFs, S-1 Approval and Trading Expected in Coming Weeks

Gensler Writes Letter in Strong Opposition of FIT 21

Congress Passes Landmark Crypto Regulatory Bill FIT 21, Garnering 71 out of 213 Democrat Votes

Congress Passes Bill to Ban Fed from Issuing a CBDC, Garnering 3 Democrat Votes

Biden Campaign Said to Reach Out to Key Crypto Industry Leaders for Guidance

Treasury Secretary Nelson States They Will Not Ban Crypto Mixers, Wants to Enhance Privacy Without Enabling Terrorist Financing

SEC Tells Spot ETH ETF Issuers to Get First Round of Draft S-1’s in by May 31st

BTC ETFs Have $2.1bn of Net Inflows

BTC ETFs File 13Fs – 563 Professional Firms Hold $3.5bn, Shattering Prior Record for ETF Launches; Retail Owns >90%

9th Largest US Pension Fund State of Wisconsin Owns $99mm BTC ETF; Millenium Owns $2bn, Susquehanna Owns >$1bn

$200mm Market Cap, Publicly Traded Tech Company Semler Scientific Purchases $40m of Bitcoin on Balance Sheet

Mt Gox Transfers $9.4bn of BTC, Presumably in Advance of Partial Distribution to Creditors

SEC Issues Wells Notice to RobinHood Regarding Crypto Business

DOJ Arrests Two Brothers for Maliciously Attacking the Ethereum Blockchain and Taking $25mm, in first ever case

Michael Sonnenshein Steps Down as Grayscale CEO, Replaced by Former Blackrock Executive Peter Mintzberg

NYSE Partners with CoinDesk to Launch Cash-Settled Index Options on the CoinDesk Bitcoin Price Index

Judge Orders SEC to Pay $1.8mm in Legal Fees in DebtBox Case

Crypto Social Media Platform Farcaster Raises $150mm from Paradigm, A16Z, et al

Bitcoin Staking Protocol Babylon Raises $70mm from Paradigm, Bullish, Polychain, et al

Binance Fired Its Head of Compliance for Flagging DWF’s Suspected Market Manipulation

DOJ Chooses FRA Over Sullivan & Cromwell for Binance Monitor

Vanguard Hires New CEO Salim Ramji, Who Appears to Favor BTC ETFs

FTX Estate to Repay 100% of Claims at Petition Date Pricing Plus Interest, Some Creditors Unhappy, Pushing for More

Japanese Crypto Exchange DMM Bitcoin Hacked for $305mm

Former FTX Executive Ryan Salame Receives 7.5 Year Sentence

FalconX Settles with CFTC for $1.8mm for Providing Access to Crypto Derivatives for US Firms

| Asset Class | May | Apr | Q1-24 | YTD | Q4-23 | Q3-23 | Q2-23 | Q1-23 | 2023 | 2022 | 2021 | Instrument |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Bitcoin | 11% | -15% | 69% | 60% | 57% | -12% | 7% | 72% | 155% | -64% | 60% | BTC |

| NASDAQ | 6% | -4% | 8% | 10% | 14% | -3% | 15% | 21% | 54% | -33% | 27% | QQQ |

| S&P 500 | 5% | -4% | 10% | 11% | 11% | -4% | 8% | 7% | 24% | -19% | 27% | SPX |

| Total World Equities | 5% | -4% | 7% | 8% | 10% | -4% | 5% | 7% | 19% | -20% | 16% | VT |

| Emerging Market Equity | 2% | 0% | 2% | 4% | 6% | -4% | 0% | 4% | 6% | -22% | -5% | EEM |

| Gold | 2% | 3% | 8% | 13% | 12% | -4% | -3% | 8% | 13% | -1% | -4% | GLD |

| High Yield | 1% | -2% | 0% | -1% | 5% | -2% | -1% | 3% | 5% | -15% | 0% | HYG |

| Emerging Market Debt | 2% | -3% | 1% | -2% | 8% | -5% | 0% | 2% | 5% | -22% | -6% | EMB |

| Bank Debt | 0% | 0% | -1% | 1% | 0% | 1% | 1% | 3% | -7% | -1% | BKLN | |

| Industrial Materials | 3% | 12% | -2% | 10% | -5% | 7% | -11% | 4% | -6% | -13% | 29% | DBB |

| USD | -2% | 2% | 3% | 5% | -5% | 3% | 0% | 0% | -2% | 8% | 6% | DXY |

| Volatility Index | -17% | 20% | 4% | 26% | -29% | 29% | -27% | -14% | -43% | 26% | -24% | VIX |

| Oil | -5% | 0% | 18% | 18% | -18% | 27% | -4% | -5% | -5% | 29% | 65% | USO |

SOURCE: TRADING VIEW. AS OF 5/31/24.

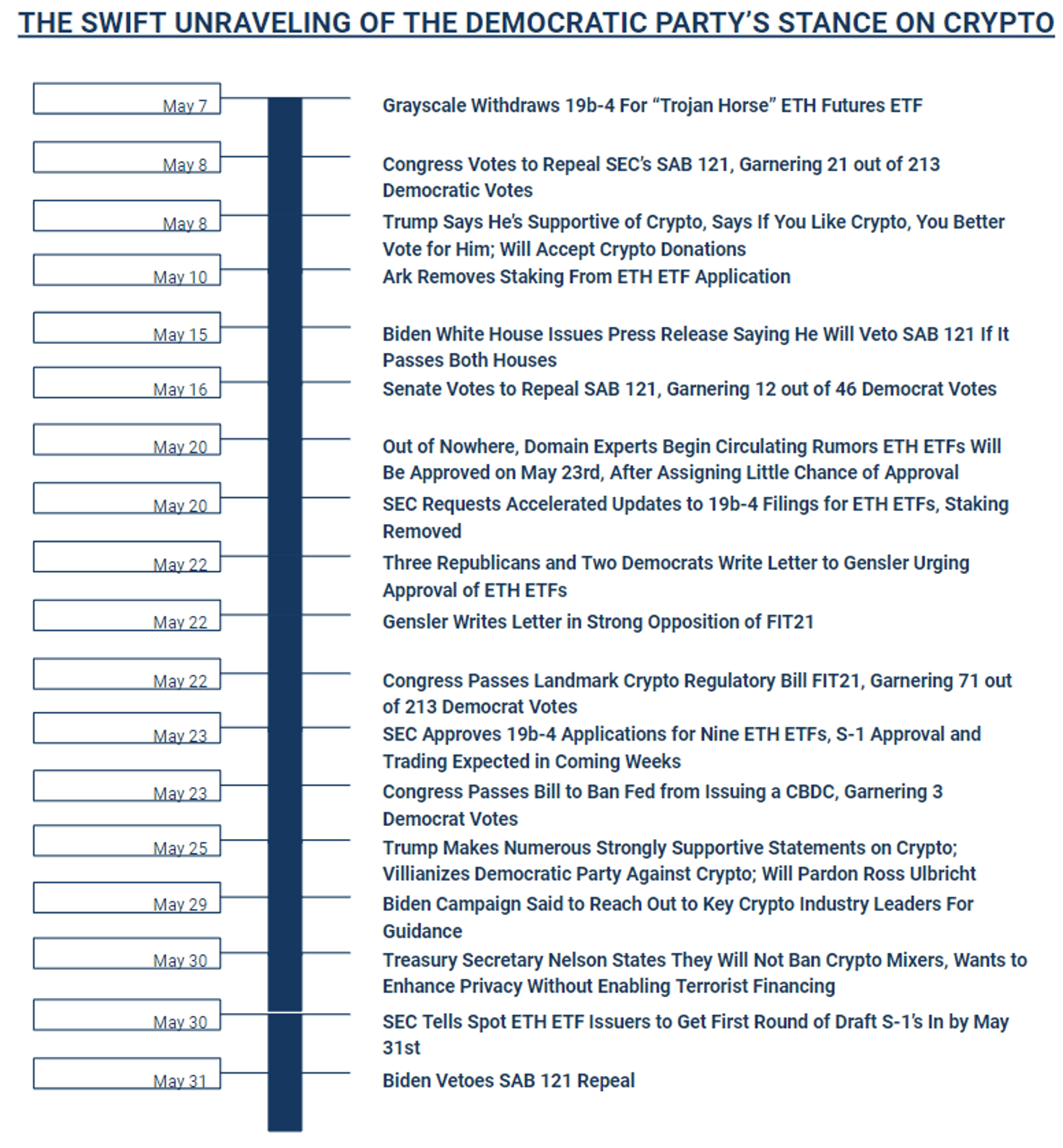

The Swift Unraveling Of The Democratic Party’s Stance On Crypto

Let’s just start with this. I don’t know how much you pay attention to crypto, but even if you pay a TON of attention to crypto (me), it’s still helpful to see it all in one place-

I mean, wow, right? So what actually happened?

The above chart is just a list of events. There isn’t conjecture in that chart. What will follow will be conjecture and maybe some predictions and those could very easily be dead wrong.

This is what it seems like might have happened -

It seems that Gensler overstepped his boundaries with SAB 121 and issued an edict he didn’t have the right to issue. It seems that it pissed off some important people, notably Wall Street, who want to profit from crypto. SAB 121 was so hurtful to Wall St, and Wall St firms were watching Larry Fink CRUSH IT on the ETFs, and they started making noise back to their Democratic puppets to fix this. This caused Democrats to break party lines and vote to repeal SAB121. Given how politicized Gensler is for the Democratic party (he is a lackey for Warren and everyone knows it), it is easy to imagine this majorly ruffling some feather inside the Democratic party.

Either right before or right after the House SAB 121 vote, someone got in Trump’s ear (Selkis is that you?) that crypto was a real opportunity for him to raise money and get votes. Someone told Trump that crypto folks are rich. Someone told Trump that supporting crypto was all upside and no downside- no one was going to vote against him for being pro-crypto, but many would vote for him just because he was pro-crypto. Trump ran with it.

My guess is this shift from Trump pressured Democrats further and additional unraveling ensued. Trump is leading in the polls and leading on the betting sites. Someone must have pulled the fire alarm internally in the Democratic party. Dems had already mostly lost faith in Gensler. Gensler had a BAD year last year. You could imagine a message going around internally with Dems –

“We’re getting killed in the polls. Trump is supporting crypto. This moron Gensler is picking fights he can’t win with crypto, and now even Wall Street is pissed about it. He already lost BTC ETFs and he’s about to lose ETH ETFs publicly and shamefully. All he’s doing with crypto is driving dollars and votes away. He’s not getting any more dollars or any more votes. Stop this madness now.”

I won’t pretend to know the layout of the Democratic party factions, but some kind of schism MUST have occurred for Biden’s people (he is unable to effectively communicate on his own) to have come out with that SAB 121 veto press release the DAY BEFORE the Senate voted to overturn it and send it to his desk. Biden has until June 3rd to veto the SAB 121 repeal, or it automatically becomes effective. Based on the timeline above, I would have been inclined to think that Biden wouldn’t veto and would let the repeal go through. But just as I was finishing up this monthly on the evening of the 31st, Biden announced he was vetoing the repeal of SAB 121. That’s disappointing, and points to the magnitude of the divide within the Democratic party right now as it relates to crypto. Apparently, Biden is going to veto a bill that 21 out of 213 congressmen and 12 out of 46 senators voted for. Not sure what to make of that. Up until 10 minutes ago when the news broke, I would have guessed the opposite.

It seems the schism in the Democratic party had immediate downstream knock-on effects. Two business days (plus a weekend) after the SAB 121 Senate vote, Gensler appears to be forced to approve the ETH ETFs. Some will argue this was always going to be the case – that the ETH ETFs were always going to get approved on May 23rd because the SEC didn’t have a leg to stand on to deny them. That would not be my base case. It seems something political changed drastically right before the May 23rd deadline. A week prior, the ETH ETFs were going to be delayed until at least August. Until Gensler got the tap on the shoulder and was essentially forced for political reasons to rush the approval of ETH ETFs.

We’ll see how long it takes to actually get the S-1’s approved and the ETFs launched. My guess is it’s somewhere between two weeks and two months and maybe consensus is it happens end of June. The SEC said they wanted first round draft S-1’s back by Friday May 31st, so that feels like a pretty accelerated timeline. We’ll see how quickly the SEC provides comments on those in the coming days and weeks.

In the meantime, Trump continued to speak out strongly in favor of supporting crypto, and the cracks in the Democratic party’s stance towards crypto continued to widen. Full disclosure, I was not following FIT 21 closely because it was my understanding that it had virtually zero chance of passing the House and even less of getting through the Senate. But sure enough, on the day Gensler writes a letter strongly opposing FIT 21, 71 out of 213 Democrats vote in favor of the bill and it passes to goes to Senate.

FIT 21 is by no means a perfect bill in its current form. These tweets are helpful in framing some of the changes you’d like to see made to FIT 21 in the Senate. I don’t think it’s anyone’s expectation that this bill will get to a vote in the Senate in its current form. And the political winds are so dynamic at the moment, that it’s difficult to have a sense of how much Dems and Reps can come together to work through changes in the bill. If the changes are substantial, which they likely would be, FIT 21 would then go back down to the House for another vote. So this is what we will be watching closely in the coming months. My guess is – observing the behavior of Democratic Senators as it relates to working through FIT 21 changes may be the best place to glean insight into the changes that have occurred in the Democratic party as it relates to crypto. I don’t know how to weigh the likelihood that we get a FIT 21 passed into law before the elections. Honestly it feels like a bit of a stretch but maybe that’s just Pavlovian. But I do know it’s a lot higher than it was a few weeks ago (when it was essentially zero). The whole thing is still very much up in the air – too much political change came out of left field too fast to have a firm grasp on the situation.

The last tangential but certainly relevant event to this wild story is Trump being convicted of 34 felonies on May 30th. His sentencing is scheduled for July 11th. I won’t pretend to have the answers about how exactly this will play out. It is my understanding that jail time is unlikely. House arrest is possible. There will be an appeal. I don’t know the exact timeline of the appeal process or the likelihood of its success. Biden’s team have said Trump will be the Republican nominee for president regardless of the conviction, so there doesn’t seem to be a path where this conviction prevents Trump from being on the ballot in November.

In the immediate wake of the conviction, there have been many pundits on both sides of the aisle stating that this conviction is decisively positive for Trump’s reelection chances. That the conviction will serve as a rallying point. I don’t have a strong view on that, and we still have a ton of time between now and the election. A month ago, a second Biden term was decidedly negative for crypto. Fast forward to today, and a Trump win in November is even MORE bullish crypto than previously expected, but it appears a Biden second term may not be nearly as negative for crypto as previously expected. That’s what we call a win-win!

Market Update – Liquid Crypto Asset Investing

| Symbol | May | Apr | Q1-24 | YTD | Q4-23 | Q3-23 | Q2-23 | Q1-23 | 2023 | 2022 | 2021 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| BTC | 11% | -15% | 69% | 60% | 57% | -12% | 7% | 72% | 155% | -64% | 60% |

| ETH | 25% | -17% | 60% | 65% | 37% | -14% | 6% | 52% | 91% | -67% | 399% |

| XRP | 4% | -21% | 2% | -16% | 19% | 9% | -12% | 58% | 81% | -59% | 278% |

| BCH* | 4% | -37% | 121% | 45% | 33% | -24% | 117% | 16% | 157% | -75% | 6% |

| EOS | 7% | -31% | 30% | -4% | 45% | -22% | -37% | 38% | -2% | -72% | 17% |

| BNB | 3% | -5% | 94% | 90% | 45% | -10% | -24% | 29% | 27% | -52% | 1269% |

| XTZ | 5% | -35% | 40% | -4% | 47% | -15% | -28% | 56% | 39% | -84% | 116% |

| XLM | -1% | -24% | 9% | -18% | 15% | 1% | 1% | 55% | 81% | -73% | 108% |

| LTC | 5% | -24% | 44% | 14% | 10% | -39% | 21% | 28% | 4% | -52% | 17% |

| TRX | -6% | -3% | 14% | 4% | 21% | 16% | 27% | 10% | 98% | -28% | 181% |

| Aggregate Mkt Cap | 13% | -17% | 63% | 53% | 51% | -6% | 1% | 49% | 119% | -64% | 186% |

| Aggregate DeFi* | 27% | -26% | 47% | 38% | 72% | -5% | -5% | 50% | 132% | -77% | 581% |

| Aggr Alts Mkt Cap | 16% | -20% | 58% | 47% | 53% | -2% | -5% | 33% | 90% | -64% | 479% |

SOURCE: COINMARKETCAP AND COINGECKO. AS OF 5/31/24. BCH INCLUDES SV.

BTC was +11% in May and now up 60% YTD, closing out May ~8% away from ATH. ETH had a big month, for obvious reasons - +25% on the month and +65% YTD, now outperforming BTC slightly YTD. Most Alts performed somewhere between BTC and ETH in May, although SOL was a notable outperformer, +30% in May.

I would argue BTC’s performance in May was actually a bit sluggish relative to the ETF inflows - $2.1bn in May I would have thought would be enough to get a new ATH. My best guess is that the ETH news induced significant BTC sell pressure (to buy ETH), that somewhat neutralized the strong BTC ETF inflows. I could imagine that setup remaining present in June as well as we march towards spot ETH ETFs.

A month ago, when we were worried about Fed rate cuts (or lack thereof), I included this chart-

Source: Tradingview. As of 4/30/24.

A month later, I don’t think the above chart is the best way to characterize the setup on BTC now. There is still risk to the two rate cuts currently priced in, but that risk has diminished relative to a month ago. It seems that the renewed BTC ETF inflows came lockstep with macro turning risk-on, so assuming inflation/labor data stays relatively soft this summer, I think BTC ETF inflows will continue to be supportive. That makes me less confident that BTC will actually stay in this range all summer (shown in yellow above). Add to that the enormously positive month crypto just had from a regulatory/political perspective, and the whole space now has meaningfully more tailwinds than it had just a month ago.

On one hand I can imagine BTC remaining in its three-month range during June due to the ETH ETF hype weighing some on BTC price action. On the other hand, the chart looks pretty ready to break out, and BTCUSD didn’t trade particularly bad as the ETH ETF event was unfolding.

All things considered, below is my base case for BTC at the moment –

Source: Tradingview. As of 5/31/24.

As mentioned above, I could imagine the yellow range actually breaking out in June, which would just pull this chart forward a bit. The greatest downside risk remains macro – inflation/labor data turns hot, cuts come off the table, Powell spooks the market, risk across the board dumps. It could happen, but not my base case at the moment.

Below is ETHBTC, a chart that looks waaaay better than it did a month ago -

Source: Tradingview. As of 5/31/24.

ETHBTC on Coinbase had its largest weekly volume candle since the very top of the range three years ago. The chart is now on the precipice of breaking out of its 18-month downtrend. I think it’s a safe assumption that breakout will likely occur in June due to the ETH ETFs.

From there, ETHBTC will likely be beholden to the ETH ETF inflows, and that is a really tough one to gauge. I struggle to come up with a base case for the first week/month/quarter inflows to ETH. There are ways you can make a guess based on BTC ETF inflows – adjust those numbers down by relative market cap, or by CME open interest, or by trading volume, or by GBTC/ETHE relative size. But I’m not sure how accurate any of those methodologies will be. The BTC ETF inflows did ~$5.1bn of net inflows in the first 30 trading days. Recall that number blew all estimates out of the water – it was a tremendous upside surprise. So how much anchoring to that number is appropriate when thinking about ETH ETF inflows?

It's a tough call. I think 10% of that $5.1bn, call it $500mm, in the first 30 trading days would be a disappointment for ETH ETFs. Price would be flat-to-down in that scenario I think. $1bn of inflows in the first 30 days should be supportive for price, that should get us knocking on the door of ATHs in ETHUSD, which is +27% from here. Beyond $1bn of inflows in the first 30 days, and ETH should really be moving. I would expect ETHUSD to new ATHs and ETHBTC back to the middle of the range (white box) above. ETH has always been a lot more jumpy than BTC, and I think that could easily play out in the coming months.

Beyond the ETFs, ETH’s investment case continues to struggle. ETH REALLY needs a new narrative – preferably one that drives mainchain activity and thus juices the burn.

The ETH fees have been quite sluggish relative to the prior bull market –

As of 5/31/24.

ETH’s burn is shown below. You can see that two months ago, the line started slopping up, which means ETH is very mildly inflationary at the moment.

Source: ultrasound.money. As of 5/31/24.

If the ETH community can figure out a way to drive mainchain transaction volume and get the burn up to say 5% annualized, I think that’s a narrative the market will grab hold of. The burn mechanism is inherently reflexive, and ETH ETF inflows are inherently reflexive. You get both of them going at the same time and it’s… reflexively reflexive! And that sounds like number go up. TBD on where that required use case is going to come from in the near term.

If BTC and ETH become ETF buddies next month, where does that leave Alts? A month ago, Aggregate Alt Mkt Cap was a chart in trouble-

Source: Tradingview. As of 5/31/24.

Agg Alt Mkt Cap had just been crushed in April, -26% on the month. And appeared to have broken through support (white box), retested prior support as resistance, and then failed at that new resistance. A month later and the chart is healthier. The support-turned resistance (white box) was broken through, price failed at a logical high resistance point (orange box) and is now retesting the white box as support. Additionally, you have a trend line (yellow) forming.

It would not be my base case to expect fireworks from this chart. It can get pulled up with positive performance from BTC and ETH, but I would expect Alts to generally lag BTC and ETH in the coming months. It’s still a pretty narrative-less situation and there are few signs of meaningful inflows into Alts broadly. Depending on how the crypto political situation shakes out – whether that’s progress on FIT 21 or Biden and Trump competing on who can be the most supportive of crypto, you could get a good uplift in Alts from that tailwind. But I think that might be later on this year as we get closer to the election.

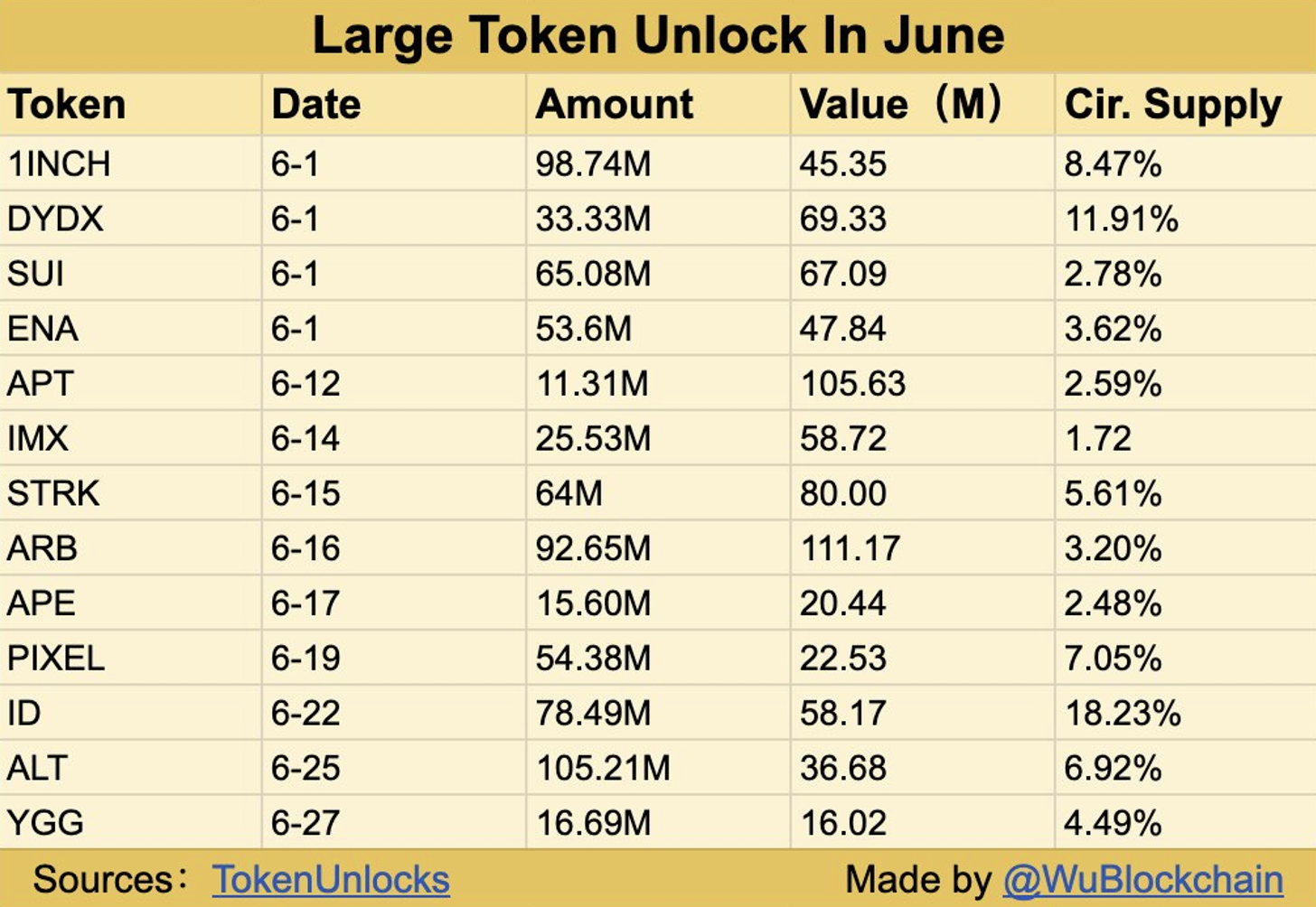

In the near-term, Alts have a token unlock issue, to the tune of $739mm in June-

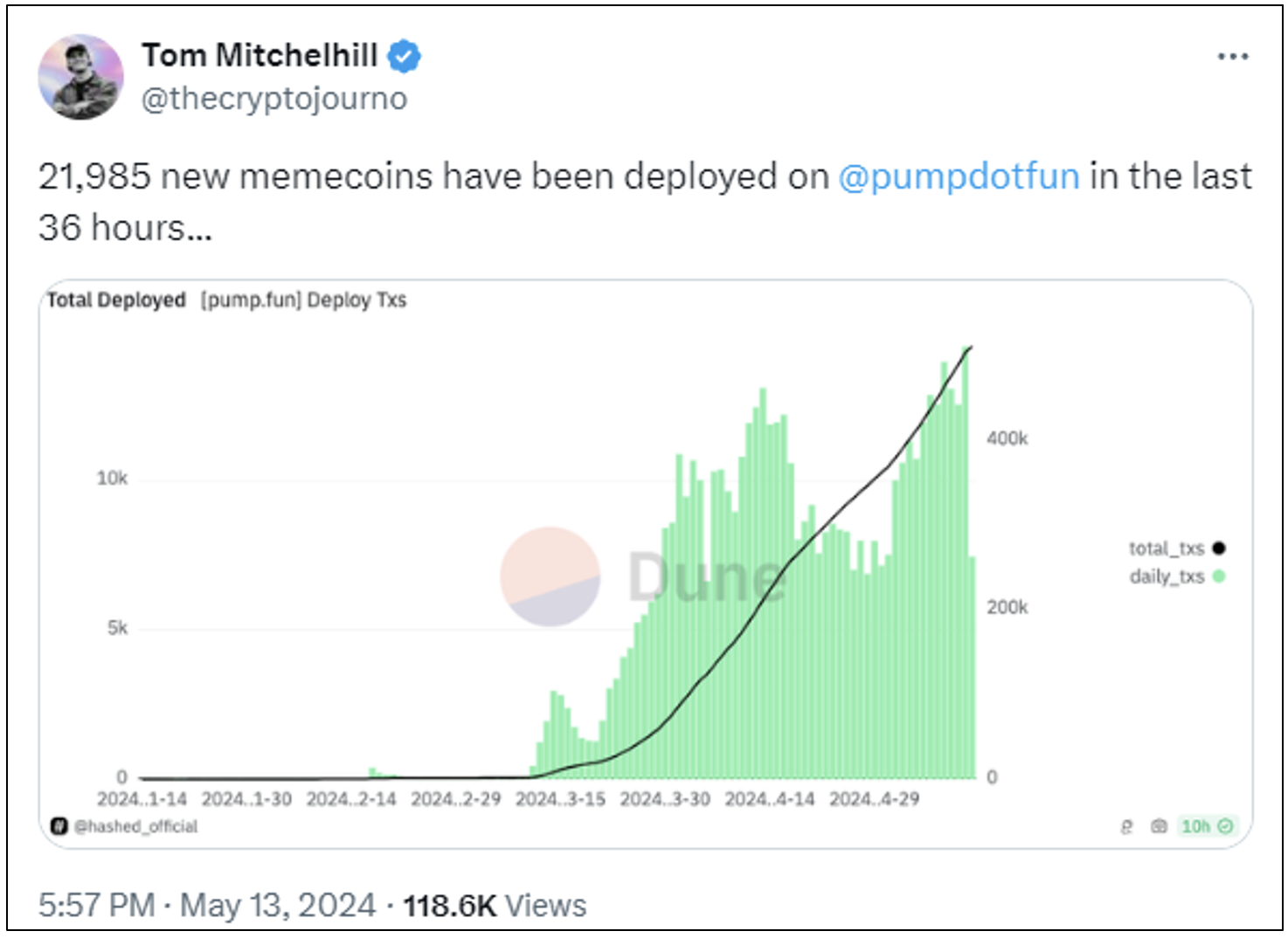

With billions more in unlocks to come in the 2H. Alts also have a new project dilution problem. Not to mention a ridiculous memecoin dilution problem-

Finally, despite strongly positive idiosyncratic news for crypto, it’s noteworthy that May was a month of “It’s All One Trade”. NASDAQ vs BTC-

Source: Tradingview. As of 5/31/24.

Closing Remarks

May was just a good ol’ fashioned enormously positive surprise. You gotta embrace those when you get them in crypto - they’ve been a bit hard to come by lately. This one in particular was particularly fun because it was just so unexpected.

This surprise we got handed to us in May certainly helped to shift market sentiment, which had turned rather sour as of late. This strongly positive regulatory/political month that crypto just had was a bit of a fresh coat of paint on a house that still ain’t built all that well. It’s an external positive catalyst that does not have an impact on the internals of crypto, at least not immediately. What I mean by that is, we’re getting ETH ETFs, but ETH still struggles with its value proposition and underlying use cases. The ETFs don’t change that. The ETH ETFs might get strong inflows (mostly because people are looking for juice everywhere) and ETH may very well rip to the high heavens, but it won’t be because the Ethereum blockchain is providing some enormously useful product or service to millions of people. Not in the near term I don’t think.

The same is generally true for FIT 21. There’s a chance it gets passed into law before the election. I wouldn’t hold my breath on that but maybe. And I think in general, the likelihood for sensible crypto legislation being passed in 2025 has increased meaningfully this month (although the elections will matter a lot for those odds). And maybe we get good legislation and that gives clarity around token structure that allows projects to create a token that has more value accruing features vs so many of the worthless token structures we’ve had for so many years in crypto. And that will be a good thing. BUT YOU STILL NEED TO PROVIDE SOMETHING OF VALUE TO THE WORLD TO HAVE SUSTAINABILITY OVER THE LONG TERM.

And that remains an issue for crypto, just like it was a month ago.

“One man’s fault is another’s lesson”

-Japanese Proverb

Travis Kling

Founder & Chief Investment Officer

Ikigai Asset Management

P.S.

Included below is an incomplete list of memorable tweets from the last month. Twitter is not investment advice and my views could easily be wrong. That being said, like it or not, Twitter matters for crypto. I have no interest in being a talking head for a living and babbling about on Twitter is a long way away from being a good steward of investor capital. However, this is a community with open-source software in its DNA, and participants want to crowd-source the truth. We are shepherds of this technology. Answers to fundamental questions about this asset class are not currently clear, so having a public platform to share your views with the community is important. After all, you’re helping shape the future :)

1. Ikigai Asset Management is the trade name for a collection of advisory and consulting businesses operated by Travis Kling, Anthony Emtman, and their team.

The information contained or attached herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. This presentation may contain forward-looking statements that are within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements are based on management’s beliefs, as well as assumptions made by, and information currently available to, management. Although management believes that the expectations reflected in these forward-looking statements are reasonable, it can give no assurance that these expectations will prove to be correct. This email is for informational purposes only and does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product, service of Ikigai as well as any Ikigai fund, whether an existing or contemplated fund, for which an offer can be made only by such fund’s Confidential Private Placement Memorandum and in compliance with applicable law. Past performance is not indicative nor a guarantee of future returns. Please consult your own independent advisors. All information is intended only for the named recipient(s) above and is covered by the Electronic Communications Privacy Act 18 U.S.C. Section 2510-2521. This email is confidential and may contain information that is privileged or exempt from disclosure under applicable law. If you have received this message in error please immediately notify the sender by return email and delete this email message from your computer. Copyright 2023 Ikigai Asset Management, LLC. All Rights Reserved.

NOT INVESTMENT ADVICE; FOR INFORMATION ONLY

PAST PERFORMANCE IS NOT A GUARANTEE OF FUTURE RESULTS