November 2019 - Market Update

/Monthly Update || November 2019

“At important turning points, when the future stops being like the past, extrapolation fails and large amounts of money are either lost or not made.”

Opening Remarks

Greetings from inside Ikigai Asset Management1 headquarters in Marina Del Rey, CA. We welcome the opportunity to bring to you our fourteenth Monthly Update and hope these are helpful in better understanding some of what we’re doing and what we’re seeing. We have the privilege of deploying capital on behalf of our investors into a new technology and asset class that we believe will fundamentally change the world and create trillions of dollars of value in the process.

We believe we are obligated to be shepherds of this technology – to help the world better understand the powerful potential of DLT and crypto assets, and to fund and be an ambassador for DLT projects that will change our lives forever.

To that end, October events and ensuing price action were nothing short of breathtaking. As a career investor in traditional asset classes prior to jumping into crypto and founding Ikigai, I have plenty of experience with catalysts and market movements. Nothing moves like crypto. I can’t imagine a technology or asset class that could so quickly become so firmly entrenched in the global macro landscape while remaining still in a state of relative infancy. Said differently, we have SO much further to go and crypto/DLT are ALREADY front and center of global stage. This. Thing. Is. Never. Going. Away.

October was a tale of two months – weak price action that brought a lower low on relatively low volumes on the back of negative newsflow in the first three weeks, followed by a stunning explosion higher on 10/25 that saw solid follow-through into month-end. At its trailing 24-hour intraday peak, 10/25 was the THIRD LARGEST price gain in BTC history. The 25th ended the day +16%, the 45th best daily performance in BTC history, a top 1.3% performance. That explosion higher came in response to a fundamental news event that may very well end up being a pivotal moment in the crypto history books. In a widely televised speech, China President Xi Jinping said, “major countries are stepping up their efforts to plan the development of blockchain technology. Greater effort should be made to strengthen basic research and boost innovation capacity to help China gain an edge in the theoretical, innovative and industrial aspects of this emerging field.” We will dive more into this situation below.

Despite the 10/25 fireworks, overall interest levels in crypto have appeared to wane in the last few months, and its too early to tell if the price move last week will reignite enthusiasm from those not already committed to the industry. We’re not exactly sure why these interest levels plateaued in early July and began declining, but we’re seeing and hearing anecdotal evidence from numerous sources. New projects raising capital has slowed. Incremental project innovation has slowed. Crypto fund AUM growth has slowed. Trading volumes had slowed (prior to the 25th). We believe this broad waning in interest may be because there is confusion about value propositions across the ecosystem – from equity investments to fund investments to Alts. We believe this waning may be because of poor messaging from the crypto ecosystem to the “pre-coiners” – an example of Metcalfe’s Law sputtering out. We believe this waning may be because of a global dollar liquidity shortage. Lastly, we believe this waning may be because of decreased risk appetite due to slowing global GDP growth and upheaval in the traditional VC landscape. More on that below.

Regardless of the why, we believe declining interest levels on the margin are transitory. 2020 will undoubtedly be a bigger year for crypto than 2019, and there’s good reason to believe 2021 will be bigger than 2020. The trajectory of this technology and asset class is exceptionally strong, whether that materializes next month or some time shortly thereafter.

October Highlights

China President Xi Publicly Supports Blockchain Innovation

Congress Holds Hearing with Mark Zuckerberg on Libra and Data Privacy

Congressmen Ask Fed to Consider Developing A Digital Dollar

Two Senators Write Ominous Letter to Libra Members Advising They Leave

Paypal, Mastercard, Visa, eBay, Stripe, et al Leave Libra Project

Two Senators Write Supportive Letter to Libra Members

SEC Issues Formal Rejection to Bitwise for Bitcoin ETF

SEC Obtains Restraining Order to Prevent Telegram Token Issuance

SEC, CFTC & FinCEN Issue Statement Warning of AML/KYC Obligations

Uber Announces Uber Money Financial Services Platform

Morningstar Announces Plans to Launch Credit Rating System on Ethereum

Ontario Securities Commission Approves Bitcoin ETF Offering From 3iQ

IRS Issues Crypto Tax Guidance

Morgan Creek Raises $61mm Led by Public Pensions

Chainanalysis Helps DoJ Shut Down Largest Child Porn Site Ever

| Symbol | October | Q3-19 | Q2-19 | Q1-19 | YTD | % ATH | % Off Low |

|---|---|---|---|---|---|---|---|

| BTC | -11% | -23% | 164% | 10% | 146% | -54% | 187% |

| ETH | 2% | -38% | 105% | 6% | 38% | -87% | 120% |

| XRP | 16% | -35% | 28% | -12% | -16% | -92% | 15% |

| BCH | 31% | -47% | 154% | -1% | 75% | -90% | 265% |

| EOS | 11% | -49% | 38% | 63% | 28% | -86% | 106% |

| BNB | 26% | -51% | 86% | 182% | 225% | -19% | 370% |

| XLM | 6% | -41% | -3% | -5% | -42% | -93% | -12% |

| LTC | 5% | -54% | 101% | 99% | 93% | -84% | 155% |

| TRX | 37% | -55% | 36% | 25% | 6% | -93% | 81% |

| Aggregate Mkt Cap | 11% | -29% | 117% | 14% | 95% | -70% | 142% |

| Aggr Alts Mkt Cap | 11% | -40% | 68% | 18% | 31% | -86% | 77% |

Forest, Not Trees

With the torrid pace of developments across the crypto ecosystem, its easy to become mired in the trees and lose sight of the forest. October was a month that reminded us of how the forest is looking. With that said, three things we want to touch on:

· Monetary Policy

· China

· Traditional VC

Monetary Policy

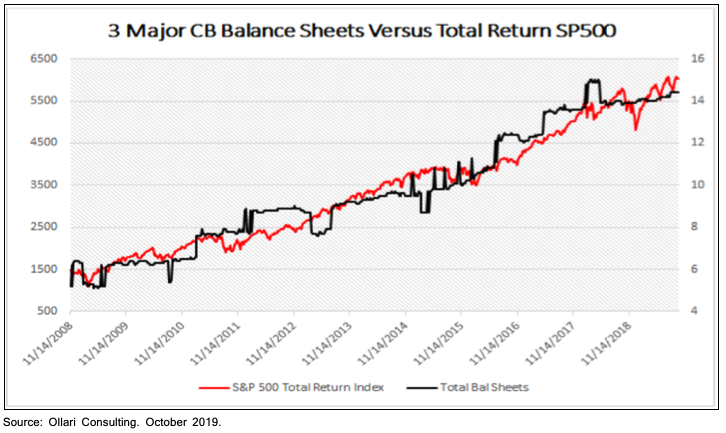

Last month, I said, “I have gone pretty far down the rabbit hole on this dollar shortage situation, listening to viewpoints from investors much more knowledgeable about the intricacies than I am. There are smart folks on both sides of the fence – some say its transitory and is already getting better. Some say the issues will last through year-end as the Fed continues to issue piles of Treasuries to refill their cash balances after raising the debt ceiling, sucking up all the dollar supply. Still, others say it won’t get better until the Fed starts juicing full-blown QE.”

Welp. Fed actions in October increased our conviction that they indeed will be exceedingly accommodative. On Oct 11th, after alluding to impending balance sheet expansion in prior weeks, the Fed introduced a $35bn POMO (conducted twice a week), $75bn TOMO (conducted daily) and $60bn of Treasury purchases (conducted monthly). Jay Powell went through great pains to describe this as “not QE”, but a technical adjustment. Let me be clear, this is Quantitative Easing. Not in the exact same manner or to the same degree as QE 1, 2 or 3, but this is balance sheet expansion via asset purchases. Looks, walks and talks like a duck. On October 23rd, the POMO was expanded to $45bn and the TOMO was expanded to $120bn. On October 30th, the Fed cut rates 25bps for the third consecutive time.

While stating they are remaining data dependent, it is apparent the Fed is going to be accommodative with its monetary policy by any means necessary. Importantly, during the press conference, Powell referenced the need for Congress to pick up the baton on the fiscal policy side with a pointedness he has not previously employed. This urgency by the Fed of moving from monetary policy accommodation to fiscal policy accommodation is mirrored by the ECB, who just appointed Christine Lagarde as Chairman. Lagarde isn’t a monetary policy expert, she’s a fiscal policy expert. The ECB has to figure out how to spend all those Euros they’re printing to keep this party going. The BoJ is no different, delivering the message this month that they will be accommodative by any means necessary.

Why are central banks doing this? Because 1) the whole world is slowing down; 2) the US stock market has become the main indicator for the health of the US, and thus global, economy; and 3) the stock market needs its drug.

Risk assets responded favorably to this backdrop in October, with the SPX reaching new ATHs, VIX collapsing from 20 to 13, yields moving higher and DXY moving lower. We doubt it is coincidence that the explosive move higher in crypto prices came two days after the Fed restarted QE and two days after they expanded repo operations to provide additional accommodation, just like we doubt it was coincidence the crypto market bottomed on Feb 8th, nine days after the Fed’s dovish capitulation.

China

US/China relations broadly, and trade agreement/tariff wars specifically, are the single largest global macro factors in existence today. It is apparent that global GDP growth is slowing at least in part because of the tariffs that have already been put in place and the uncertainty around what the future may hold in that regard. Global financial markets whipsaw around every tweet from Trump that mentions China. If Trump doesn’t deliver on a trade deal, there is a good chance he could lose the 2020 election; if he does deliver, his re-election is highly likely. In addition to monetary easing from central banks, the “first phase” of a trade deal (which was barely a deal at all) being put in place Oct 11th was the main driver for risk assets rallying in October.

There are massive implications at stake in this situation. US/China relations are about the incumbent global supremacy fighting off a formidable challenger. It encompasses every aspect of global financial markets and economic growth. Democracy and communism. The world reserve currency. Global hegemony.

This makes Xi’s explicit public move towards blockchain innovation last week of massive importance. It has long been known that China has been working on a digital sovereign currency, named the DCEP. While China banned ICOs and the purchase of crypto with fiat in 2017 (to combat capital flight), a robust peer-to-peer crypto purchasing network has immerged in China. Chinese-controlled crypto funds moved to Singapore and served as funnels to get RMB out of the country. China-controlled mining pools account for ~80% of BTC hashpower and an estimated 40% of BTC hashpower is physically located in mainland China. Make no mistake, China has never been anything other than firmly entrenched in this technology and asset class. But now they’re open about it.

With this most recent step, much of the uncertainties and contradictions around China’s stance towards crypto and DLT have been removed:

China will launch DCEP soon. They are launching it specifically to combat capital flight and increase surveillance.

By beating the US to market with a digital sovereign currency, China hopes to make a further dent in the US dollar’s world reserve currency status – another critical and tenuous aspect to US/China relations.

China is now banning anti-blockchain sentiment in articles.

China’s most popular mobile app Xuexi Qiangguo (translation: study for becoming powerful nation) now has a recommended course focusing entirely on blockchain, including lessons on Bitcoin and Ethereum.

Chinese stocks with any involvement in blockchain skyrocketed this week.

CCTV, China’s state-controlled television, has been showing blockchain explanatory content.

A law has been passed, “The Cryptography Law”, going into effect 1/1/20, governing the treatment of cryptography IP, public/private key treatment, social public interest and more.

The Guangzhou government announced a $140 million subsidy fund to encourage blockchain development.

Wechat and Baidu searches for blockchain and Bitcoin skyrocketed on Xi’s announcement:

All of the above happened in one week. Is it coincidence all of this occurred two days after Zuckerberg’s congressional testimony on Libra? Unclear. But it is likely China views Libra as a threat to the DCEP, and for good reason. For months we have stated that getting Libra launched is a matter of national security for the US, and that’s more true today than ever before. Blockchain, Bitcoin and digital money have now been firmly inserted in the middle of the largest global macro factor in existence. This. Thing. Is. Never. Going. Away.

Traditional VC

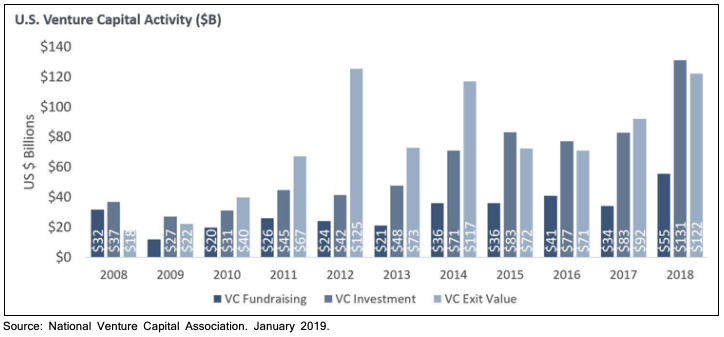

I want to be careful about opining on an area I don’t know too much about. I do not come from a VC background and have limited experience in VC investing. There are folks reading this right now that have decades of VC experience, deploying hundreds of millions of dollars into startups that have gone on to change the world. So, as a preface, I could certainly be wrong about my assessment of the current traditional VC landscape, but I’m not the only one with this view. This topic is important in the context of our Monthly Update because we believe recent trends in traditional VC have knock-on effects to the crypto ecosystem.

The WeWork debacle is the poster child for a broader set of challenges facing the traditional VC industry, and with a bit of hindsight may end up being a crescendo moment in VC that changes the trajectory of the entire industry for the coming years.

We know tech startups are staying private longer and raising bigger growth private equity rounds.

The tech companies that have IPO’d in 2019 have seen poor subsequent performance.

We know VC is getting crowded.

Especially crowded by Softbank’s Vision Fund. Which appears to have overpaid on a number of deals.

Which is causing even the best VC’s returns to suffer.

The VC industry continues to raise and deploy record amounts of capital. In many cases, these raises have come on the back of prior fund performance that is, by and large, composed of unrealized profits. With the poor performance of tech IPO’s in 2019 topped off with the WeWork dumpster fire, investors are starting to get nervous about how they’re going to realize those paper gains. For the large companies approaching another fundraising round in 2020, there is a view that those rounds will come at valuations lower than the previous rounds. All of this may be causing a shift in risk appetite as investors begin to mentally mark down their investments. To the extent this scenario continues to play out, investor appetite for early stage tech may wane, and that affects crypto. It might be affecting crypto right now.

So What?

Monetary Policy. China. Traditional VC. What’s the takeaway from all that?

The Fed just cut rates three times and juiced QE with the SPX at ATH’s and unemployment at record lows. They did it because 1) the world was slowing down; 2) China trade wars were looming (partially causing #1); and, most importantly, 3) there is a global dollar shortage.

China feels that dollar shortage as acutely as anyone and they realize that as long as the dollar has a stranglehold on world reserve currency status, they will in many ways be at the mercy of US monetary policy. They really don’t like that, and thus have been looking for ways to usurp the dollar from its throne. The petro yuan was a perfect example of that. And this new “blockchain is good” initiative, and the introduction of the DCEP, is the next example of that.

It’s apparent that the concept, definition and role of money globally is on the brink of undergoing large-scale change. Every government wants to do away with physical cash. In China it’s for surveillance and capital flight prevention. In Europe it’s to more acutely implement increasingly exotic monetary policies. Tech companies can innovate faster than governments and can better deliver on digital money. WeChat/Alipay is doing it for their government. Libra might just be doing it for the US government.

As I’ve said previously, central banks have no plan to end the largest monetary experiment in human history – quantitative easing while simultaneously running increasingly larger deficits on top of increasingly untenable debt levels. Instead of ending it, they’re just going to keep the party going and see what happens. A good friend of mine likes to say, “QE turned your savings account into your checking account, the bond market into your savings account, the equity market into the bond market, the VC market into the equity market, and crypto into the VC market”. So, to the extent QE is going to continue, it’s difficult for me to see a situation where traditional VC moves into some sort of secular bear market. A few down rounds here and there? Sure. Some realized marks that come in at a fraction of their prior-marked paper gains? Sure. But investors will increasingly be pushed out on the risk spectrum and that will drive flows into VC. Crypto is on the tail-end of all that, so flows into crypto will benefit from that.

Everything I’ve laid out above is in the context of US dollar global hegemony. It’s the dollar’s world, and everyone else is just living in it. The fate of the dollar is more or less in the hands of a handful of central bankers, and they’ve tipped their hand. They’re going to do everything they can to devalue their currency. But so are all the other central banks! So if everyone is racing to devalue their currency the fastest, what are they devaluing against? They’re devaluing against assets with provable scarcity. Gold has provable scarcity. Bitcoin has even more provable scarcity than gold. In Austrian economics terms, it’s the hardest money in human history. Bitcoin is a non-sovereign, hardcapped supply, global, immutable, decentralized, digital store of value. It is an insurance policy against monetary and fiscal policy irresponsibility from central banks and governments globally. And we’re gonna need it.

Market Update – Liquid Crypto Asset Investing

After being down more than 10% 24 days into the month, BTC came roaring back to finish October +11%, now +146% YTD. As discussed, that explosive move higher was in response to China’s about-face with regards to its public stance towards blockchain. This caused public cryptos based in China, led by Chinese founders or considered to have strong Chinese ties to rip even more than Bitcoin. NEO was up >95% at its peak. ONT >115%. IOST ~100%. QTUM >80%. Those explosive moves proved short lived though, as all the names have since walked back 20-30% from their peak and are not seeing follow-through buying volume. A friendly reminder that most Alts more than a year old have bagholders that are deeply underwater, quick to take any chance they get to unload at higher prices, squashing a rally before it even gets started. We have done full qualitative reviews of these Chinese projects. By and large they are worthless. Many are zombies, with no development or activity occurring on the network. We did not purchase any Chinese-centric cryptos on the back of this news.

As we’ve discussed previously, the acceleration we had in Q2-19 was of historic proportions, which led us to a correction of a magnitude not typically experienced in BTC bull markets before. June 26th peak to Oct 23rd trough, the correction was 47%. The entire thesis that BTC was still in a bull market was looking quite shaky on Oct 24th. But just like that, the picture changed.

After retracing approximately 62% of the entire move from Dec 2018 to June 2019, BTC found a bottom on big volume.

Was this bottom foreseeable? Few could have known about Xi’s speech before it occurred, but there were some signs. The #1 hint that a bottom was forming was how orderly we made a lower low just two days prior. September 24th was violent. Largest volume since the June 26th top. Tether price blew out. Contango blew out. BTC price spreads blew out. None of that occurred with the new low on the 23rd. Note the ho-hum volume on the lower low from the 23rd. Textbook supply exhaustion. And note the explosive volume on the move higher the 25th. Largest 4hr volume candle EVER on Bitmex. BTC changing trend in typical flashy fashion.

Can we be sure this move higher wasn’t a headfake? Not yet. But in times like these it helps to look at larger timeframe oscillators. Below is the 3D price, MACD and RSI. These look like bottoms to us.

SPX made new ATH’s in October. Gold is just off its multiyear highs. Both of these are responding to QE. As you know, we believe BTC is a macro asset, albeit a fledgling one. We think the argument can be made that BTC is cheap here relative to SPX and gold.

To the extent weak initial volumes on Bakkt were the cause of the market drop in September, the recent rate of change there has been exciting. To the extent this continues, the market will take it as a bullish signal.

For as painful as Q3-19 may have been for some crypto investors, BTC is still right on track according to the chart below. My gut tells me we may break out of the pink box before May 2020.

We’ve talked for months about the need to reset on-chain metrics after price ran too hard, too fast. That reset was well underway until the 25th but it appears done, at least for now. We continue to monitor this and other similar proprietary metrics closely.

While leveraged derivatives traders can swing price several thousand dollars in either direction just from getting offsides too much in one direction, we believe overall trends in Bitcoin are decided through the movement of large amounts of physical BTC. The 30-day circulating supply of BTC is nearing multi-year lows, while the 1D and 7D supply saw only a small uptick off of low levels on this recent move up in price. This is bullish.

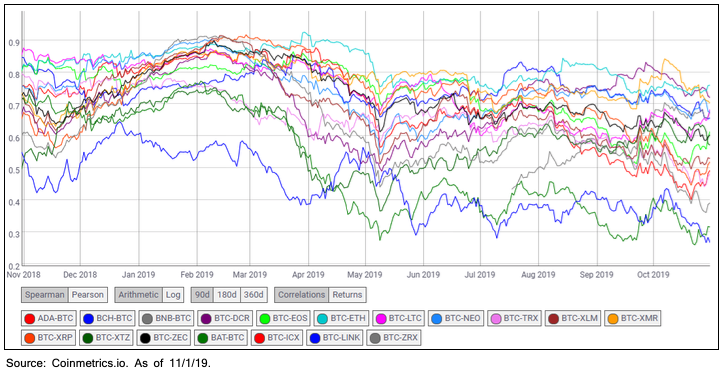

Cross-coin correlation declined in October. We view this as healthy.

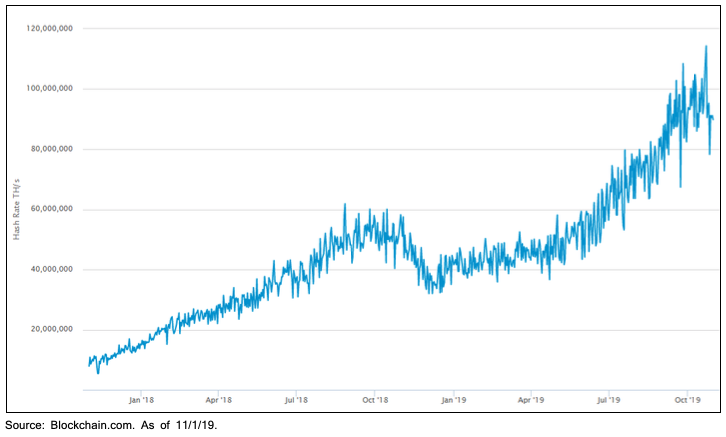

Hashrate made new ATH’s again in October and remains strongly in an uptrend. This is bullish.

Closing Remarks

After making a convincing case for the “echo bubble” thesis with lower lows and sluggish volumes through the first three weeks of October, Bitcoin came roaring back to life, courtesy of President Xi. October brought a slew of fundamental events and catalysts for crypto, both positive and negative. US politicians continue to rail on Libra, although a path to platform launch looks more likely today than it did just two weeks prior. Blockchain and digital money have moved front and center on the global stage and are planted firmly in the middle of the largest global macro situation in existence today – US/China relations. Investor appetite for crypto broadly may have waned in prior months for a number of reasons, but we believe those are likely to be transitory. QE ad infinitum will keep investors hunting for returns further out on the risk spectrum and that is to the benefit of early stage crypto projects.

Bitcoin is made possible by QE while standing outside of QE. If central bankers and politicians were more responsible with their monetary and fiscal policies, the need for a non-sovereign form of money would be diminished. If we were still on the gold standard, and governments ran balanced budgets, no one would care about Bitcoin and I wouldn’t be sitting here writing this. We would still be talking about digitizing sovereign currencies, because that’s natural technological evolution, but you wouldn’t have to worry about that sneaking feeling that whether it’s a digital dollar, a DCEP, a Libra, a digital SDR, an Alipay or a Venmo, the underlying monetary policy of that MoE is fundamentally flawed.

But that ain’t the world we’re living in.

“Adversity is the foundation of virtue.”

Travis Kling

Founder & Chief Investment Officer

Ikigai Asset Management

Invest

Ikigai is currently fielding interest from new investors. Contact us to see if you qualify.

P.S.

Included below is an incomplete list of memorable tweets from the last month. Twitter is not investment advice and my views could easily be wrong. That being said, like it or not, Twitter matters for crypto. I have no interest in being a talking head for a living and babbling about on Twitter is a long way away from being a good steward of investor capital. However, this is a community with open-source software in its DNA, and participants want to crowd-source the truth. We believe we have built a team and a process that will produce these truths more quickly and more clearly than our competitors. We are shepherds of this technology. Answers to fundamental questions about this asset class are not currently clear, so having a public platform to share your views with the community is important. After all, you’re helping shape the future :)

1. Ikigai Asset Management is the trade name for a collection of advisory and consulting businesses operated by Travis Kling, Timothy Lewis, Anthony Emtman, and their team.

The information contained or attached herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. This presentation may contain forward-looking statements that are within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements are based on management’s beliefs, as well as assumptions made by, and information currently available to, management. Although management believes that the expectations reflected in these forward-looking statements are reasonable, it can give no assurance that these expectations will prove to be correct. This email is for informational purposes only and does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product, service of Ikigai as well as any Ikigai fund, whether an existing or contemplated fund, for which an offer can be made only by such fund’s Confidential Private Placement Memorandum and in compliance with applicable law. Past performance is not indicative nor a guarantee of future returns. Please consult your own independent advisors. All information is intended only for the named recipient(s) above and is covered by the Electronic Communications Privacy Act 18 U.S.C. Section 2510-2521. This email is confidential and may contain information that is privileged or exempt from disclosure under applicable law. If you have received this message in error please immediately notify the sender by return email and delete this email message from your computer. Copyright 2019 Ikigai Asset Management, LLC. All Rights Reserved.

NOT INVESTMENT ADVICE; FOR INFORMATION ONLY

PAST PERFORMANCE IS NOT A GUARANTEE OF FUTURE RESULTS