September 2021 - Monthly Market Update

/Monthly Update || September 2021

“If everyone likes it, it’s probably because it has been doing well. Most people seem to think that outstanding performance to date presages outstanding future performance. Actually, it’s more likely that outstanding future performance to date has borrowed from the future and thus presages subpar performance from her on out.”

Opening Remarks

Greetings from Ikigai Asset Management¹ headquarters. We welcome the opportunity to bring to you our thirty-sixth (!!!!) Monthly Update and hope these are helpful in better understanding some of what we’re doing and what we’re seeing. We have the privilege of deploying capital on behalf of our investors into a new technology and asset class that we believe will fundamentally change the world and create trillions of dollars of value in the process.

We believe we are obligated to be shepherds of this technology – to help the world better understand the powerful potential of DLT and crypto assets, and to fund and be an ambassador for DLT projects that will change our lives forever.

To that end, seeing as this month marks three years of writing the Monthly Update letter, I can’t help but reminisce on how far we’ve come over that time. Anyone who’s been in crypto full-time for a while knows that this space makes time do weird stuff. Things in the past can feel simultaneously both very recent and very long ago. That’s certainly true when I think about the first one of these I wrote – it feels like just the other day and at the same time five lifetimes ago.

SO much has changed for crypto, for Ikigai and for myself personally in the last three years. Three years ago today, the entire market cap of crypto was $237bn – today it stands at just over $2 trillion – a nearly 800% increase.

Source: CoinMarketCap. As of 8/31/21.

Three years ago, Ikigai was still several months away from launching as a fund and accepting its first dollar of outside money. We had only just begun to develop strategies for deploying capital and generating attractive risk-adjusted returns. Today, we are well into nine figures of AUM and have two years of solid outperformance in our primary strategy called Programmatic Discretionary.

Three years ago, I was nine months out of Point72 and drinking from a firehose of information generated by an ecosystem that moved faster than anything I’d ever experienced previously. I knew a fraction of what I know now. I held beliefs I now know to be untrue. My brain worked differently three years ago than it does now.

All this growth that’s occurred in the last three years has come with a backdrop that has changed a lot too. The world is a DIFFERENT place than it was three years ago. Trends have changed. Communication has changed. The opinion of the people has changed. The depth and breadth of trust at all levels has changed. The traditionally accepted definition of “work” has changed. “Government” as an applied concept has changed. Because of all these factors and many more, the investing landscape is different than it was three years ago.

If I were to boil that change in the investing landscape down to one chart, it would be this chart. Green arrow was three years ago.

At risk of sounding hyperbolic, this is “the only chart that matters”. Most everything else flows from this. Not the least of which is crypto, and Bitcoin specifically. You can think about what your expectations for crypto would have been three years ago if you knew the above chart was going to be flat for three years. And you can think about what your expectations for crypto would have been if you knew that chart was going to do what it just did - go from $20tn to $30tn. Those would be two different sets of expectations.

I would argue total crypto market cap going up $1.7tn while Central Bank balance sheets went up $10tn does not strike me as overvalued. Bitcoin market cap went from $125bn to $900bn in three years while Central Bank balance sheets increased $10tn. That REALLY doesn’t strike me as overvalued. If you think that chart above has been so important these last few years, you’d find it worthwhile to think about the outlook for Central Bank Balance Sheet expansion. Expansion is set to continue for a while longer, but at a slower pace than what we just witnessed. They might even try and turn it off altogether. For a bit.

That might give some investors pause about the outlook for crypto and other risk assets in a vacuum, but at this stage it matters what fiscal policy is doing along with monetary policy. Monetary policy is set to pick up meaningfully even by conservative estimates. I’d bet these projections from the CBO will be understated over any timeline.

Source: FRED and CBO. As of 7/1/21.

So, when you look out over the next three years and the three years after that and after that, in the context of the three years we just had, its reasonable to believe crypto and risk assets broadly will have similar tailwinds to the tailwinds they’ve had. It’s true that Central Banks may very well taper asset purchases all the way to zero. They might even get a few rate hikes in (from zero or negative interest rates currently). But both of those will be short lived. A couple quarters or a year or maybe 18 months. Then the cuts will come and then more QE and that QE will be bigger than ever and more exotic than ever. By the time we get to the 2024 Bitcoin halving, there’s a good chance the printing presses will be brrring faster than ever.

That may very well be the backdrop for the next three years. Or any number of other things could certainly happen as well. That said, slow or zero growth in Central Bank Balance Sheets, deficit spending or simply M2 Money Supply is unlikely to happen at all, and highly unlikely to happen for very long.

This backdrop is likely to keep capital pouring into the crypto ecosystem at a pace that exceeds the already torrid pace we’ve experienced in the prior three years. The capital will come via all avenues – spot crypto investments, crypto equity investments, derivatives, fixed income, digital collectibles, structured products, DAOs and new ways I can’t imagine. There’s a question worth asking at the current juncture of whether $2.1tn of aggregate market cap is commensurate with the adoption this asset class currently has. I think there’s a valid case to be made that answer is no. But that’s missing the entire point and likely an incorrect approach to assessing investment in this asset class and technology. It’s about where this all may be going and the likelihood of various outcomes.

On the first page of the first one of these Monthly Updates I wrote, I said:

“…the basic thesis [is] that Distributed Ledger Technology (DLT) and Digital Assets will rearchitect the foundational layer of the internet, becoming ubiquitous to the point that we will not even notice them, in the same way we don’t notice HTTP or TCP/IP today. Through this transformation, we believe trillions of dollars in value will be created in the process.”

Three years in, that thesis is looking really good.

Invest

Ikigai is currently fielding interest from new investors globally. We are open to international investors and qualified accredited U.S. investors (including self-directed IRAs).

We accept new investors on the 1ˢᵗ and 15ᵗʰ of every month.

Contact us to see if you qualify.

August Highlights

SEC Chair Gensler Makes First Extensive Public Comments on Crypto Regulation, Stating DeFi Regulation Is Coming and Signaling an ETF Holding BTC CME Futures Through “40 Act” Structure Could Get Approval

Invesco and ProShares Immediately File For 40 Act ETFs Holding BTC CME Futures, Other Companies Follow

$1tn US Infrastructure Bill Held Up for a Week Because of Fierce Pushback from Crypto Industry on Crypto Broker Definition and Requirements

Coinbase Receives Approval to Purchase >$500mm of Crypto on Balance Sheet and Invest 10% of Profits in Crypto Going Forward

FTX US Acquires Regulated Crypto Derivatives Exchange LedgerX

FTX Partners with PR and Media Powerhouse Dolphin Entertainment to Launch NFT Platform

FTX Becomes First Derivatives Exchange to Pass a GAAP Audit

FTX Signs 7 Year Endorsement Deal with League of Legends

FTX Purchases Naming Rights to University of California’s Stadium

Microstrategy Purchases $177mm of Bitcoin at $45,294 Average Price from July 1st to August 23rd

Matrixport Raises $100mm Series C at >$1bn Valuation

Messari Raises $21mm Series A Led By Point72 Ventures, Its First Crypto Investment

FalconX Raises $210mm Series C at $3.75bn Valuation

Helium Raises $111mm in Token Sale Led by A16Z, Ribbit, Alameda, Multicoin and Others

TaxBit Raises $130mm Series B at $1.33bn Valuation, Led by Tiger Global and Paradigm

Polygon Acquires Hermez Network For $250mm in MATIC Tokens in First Ever Merger of Blockchain Networks

Blockstream Raises $210mm at $3.2bn Valuation Baillie Gifford and Bitfinex

MobileCoin Raises $66mm Series B Led by Alameda and Coinbase Ventures

TikTok Chooses Ethereum App Audius as Platform for New Sounds Library

Tiger Global Reports 2.6mn Shares of COIN

BlackRock Takes 7% Ownership Stakes in Public Bitcoin Miners Marathon Digital and Riot Blockchain

Morgan Stanley Reports Owning >1mm Shares of GBTC Across Multiple Funds

Bill Miller Reports Owning 1.5mm GBTC Shares

SEC Makes First DeFi Related Charges Against Fraudulent Company “DeFi Money Market”

BitMEX Reaches $100mm Settlement with CFTC and FinCEN

Binance Hires Former US Government Cybercrime Investigator to Lead Money Laundering Reporting

Former Head of OCC Brian Brooks Resigns as CEO of Binance US

Binance Implements Significantly Stronger KYC Requirements

Binance Singapore Hires Former SGX Chief Regulatory Officer as CEO

Walmart Hiring For “Cryptocurrency Lead” Position

Former SEC Chair Jay Clayton Joins Fireblocks Advisory Board

State Street to Offer Fund Administration Services to Crypto Funds

Coinbase Announces Explosive Q2 Quarterly Results

Substack Adds Bitcoin Lightning Payments

Wells Fargo and JPMorgan Partner with NYDIG to Launch Bitcoin Funds

VanEck and ProShares Withdraw Ether Futures ETF Proposals

Second Largest US Mortgage Lender United Wholesale Mortgage to Accept Crypto Payments This Year

USDC Decides to Hold All Reserves in Cash and Short-Dated Treasuries

| Asset Class | August | July | June | May | April | Q2-21 | Q1-21 | YTD | 2020 | Instrument |

|---|---|---|---|---|---|---|---|---|---|---|

| Bitcoin | 13% | 19% | -6% | -35% | -2% | -41% | 103% | 63% | 303% | BTC |

| NASDAQ | 4% | 3% | 6% | -1% | 6% | 11% | 2% | 21% | 48% | QQQ |

| S&P 500 | 3% | 2% | 2% | 1% | 5% | 8% | 6% | 20% | 16% | SPX |

| Total World Equities | 2% | 1% | 1% | 2% | 3% | 6% | 6% | 15% | 14% | VT |

| Emerging Market Equity | 2% | -6% | 1% | 2% | 1% | 3% | 4% | 1% | 15% | EEM |

| Gold | 0% | 3% | -7% | 8% | 3% | 3% | -10% | -5% | 25% | GLD |

| High Yield | 0% | 0% | 1% | 0% | 1% | 1% | 0% | 1% | -1% | HYG |

| Emerging Market Debt | 1% | 0% | 1% | 1% | 2% | 3% | -6% | -2% | 1% | EMB |

| Bank Debt | 0% | -1% | 0% | 0% | 0% | 0% | -1% | -1% | -2% | BKLN |

| Industrial Materials | 0% | 3% | -4% | 5% | 8% | 8% | 8% | 21% | 16% | DBB |

| USD | 1% | 0% | 3% | -2% |

-2% |

-1% | 4% | 3% | -7% | DXY |

| Volatility Index | -10% | 15% | -6% | -10% |

-4% |

-18% | -15% | -28% | 66% | VIX |

| Oil | -5% | 2% | 10% | 5% | 7% | 23% | 23% | 46% | -68% | USO |

Source: TradingView. As of 8/31/21.

A Multichain World

Last month, I wrote about venture capital pouring into crypto. The breadth. The depth. The size of the raises. The valuations. The diversity and quality of the investor base. The amount of dry powder available. I’ve been thinking more about that over the last month and one major conclusion I came to (which may be obvious to many of you reading this), is that the capital coming into this space right now is firmly making a bet on a multichain world. I would argue it’s not just a multichain world - it could be viewed as a decidedly “Low Bitcoin Dominance” world. To visualize it simplistically, Dominance is currently at 43% up slightly from a May 2021 low of 40% and not far from the all-time low in January 2018 at 36%. This Multichain World is a world where BTC Dominance continues in a secular decline from here. For years.

Source: TradingView. As of 8/31/21.

It’s a world where the aggregate market cap of Layer 1 smart contract platforms meaningfully exceeds Bitcoin’s market cap. A world where the aggregate DeFi market cap is 10x or 20x from its currently level of $127bn. A world where Layer 1’s interact seamlessly with one another. A world where OpenSea monthly volumes of $3.3bn (August 2021) is a slow month. A world with hundreds of millions of active crypto users doing things other than just holding BTC. A very different world than we live in now, but certainly not impossible to imagine three years from now.

While I was in Miami for the Bitcoin Conference in June, I took note that it was likely the most unloved I’d ever seen Bitcoin on a relative basis. And that was at a Bitcoin conference! Fast forward three months and that’s more true today than it was then. Bitcoin is SO unloved. Investors at every level seem to be “over” Bitcoin. Not enough meat left on the bone. Investors of all sizes and sophistication are looking for something with some real juice on it - the elusive 10x. Those are concepts we’ve been talking about for months here, but it’s evolved. There’s been more fuel recently added to this Multichain World fire I’m describing. Bitcoin has been labeled (whether accurately or not) as “not innovative”. Look at the public and private equity markets outside of crypto. Innovation is richly rewarded. The view of global investment markets is that innovation leads to users which leads to market share dominance which leads to customer stickiness which eventually leads to cash flows. Nearly an infinite amount of capital (more on that later) is available to fund innovation at all stages along that lifecycle. That trend is clear.

Source: Yardeni Research. As of 8/28/21.

Bitcoin is BoomerCoin. It’s boring. It NEVER changes. It doesn’t actually DO anything. It just sits there in a wallet and you don’t spend it or use it for stuff or flip it for JPEGs. It just sits there. It’s “Digital Gold”. Yuck! Gold is SO old. It’s literally the oldest investment of all time. Who wants Digital Gold? Most investors hold zero gold in their portfolio. Maybe if you’re conservative you have 50bps or 1% or 2% or if you’re a gold bug psychopath you have 15% of your portfolio in gold. And it’s rarely been more out of favor than it is now – because it was SUPPOSED to go up a lot when the Fed does three towers (slang term for “trillions”) of QE in six weeks but it DIDN’T. You know what did go up a lot? Big Tech.

Source: TradingView. As of 8/31/21.

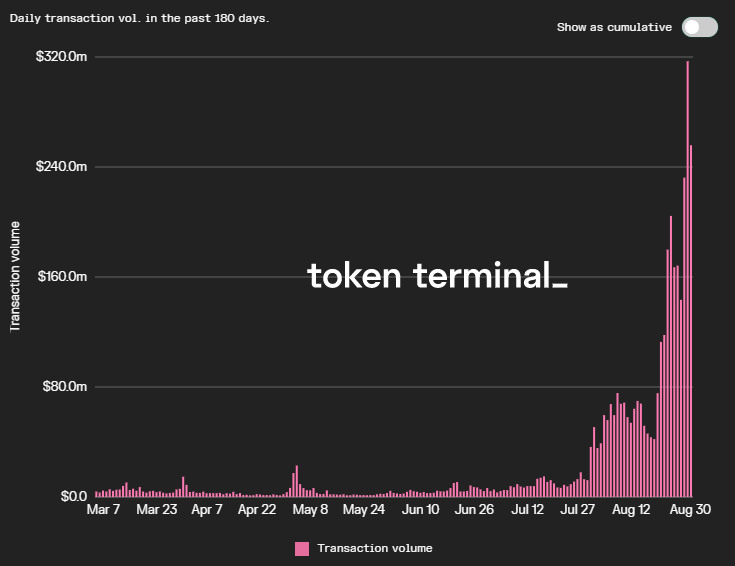

Bitcoin is gold. ETH is FAANG. Layer 1’s are Big Tech. These platforms have the flexibility to innovate until a use case really takes hold and mass adoption comes roaring into crypto. This stance has become even more compelling over the last month as NFTs have seen truly stunning activity levels. OpenSea transaction volume shown below.

Source: Token Terminal. As of 8/31/21.

Investors are looking at the current Layer 1 and Application layer landscapes and pattern matching Big Tech on top of them. You’re telling me you can buy ETH and not only get DeFi but you ALSO get NFTs? Isn’t that like buying Google and getting Search AND Email? Isn’t that like buy Facebook and getting WhatsApp AND Instagram?

Or perhaps the market is deciding ETH is also too boomer? Et tu Brute? Could be. The fees are too high! Just look at them!

Source: Token Terminal. As of 8/31/21.

Why buy ETH which might actually be A-O-L, when you can have S-O-L? Really fast transactions, nearly free transaction costs. Oh and the best executer in the space, SBF, is driving the boat. Now THAT’S got some juice on it. Want to make a broader, even more Multichain World bet? Go down market cap to other fast Layer 1 platforms. That YTD relative performance looks like this-

Source: TradingView. As of 8/31/21.

Sheesh. YTD the market has made it clear. And amazingly, off the bottom in March 2020, the relative performance is even more exacerbated.

Source: TradingView. As of 8/31/21.

This is a Multichain World. A world that rewards innovation because it’s paid off before in Big Tech. A world where you can own Layer 1’s and get the finance of DeFi with the culture of NFTs alongside the addiction of gaming plus whatever else they come up with in the future all rolled up into one. Bitcoin is so over!

Now. This stance towards the current market – with Bitcoin Dominance near all-time lows, is a stance with a decidedly stronger risk appetite relative to a world where Dominance is say, 80%. This is true in the sense that in the current low-dominance world you are paying more up front now for projects that are much younger, much less proven, with much less users, much less accessibility and much less brand recognition than Bitcoin. But potentially more utility! And certainly more innovation!

That’s what strikes me most about all this - tying back in the beginning of this Monthly Update letter’s discussion on monetary and fiscal policies, along with last month’s discussion of venture capital crypto funding. A Multichain World is being propagated by the manner in which venture capital is being deployed into this ecosystem, and that looks set to expand, not abate. That venture capital funding is being made available because of the historically loose monetary and fiscal policy we are currently experiencing, and while that looseness may abate temporarily, it is highly unlikely to abate too much for too long. If and when money supply creation does slow, it would be fair to assume the prices of all this stuff will correct and the riskiest, least proven stuff will decline the most. But it’s not like innovation in the crypto space will cease during that bear market, whatever the length may be. Hundreds of projects and companies currently have years of funding in the bank. VCs are sitting on tons of dry powder and aggressively raising more in real time. The innovation of a Multichain World will continue to be well-funded throughout the duration of any bear market that may come. All signs currently point to that being the case.

Imagine this bet - “other uses cases for crypto outside of holding BTC will gain mass adoption, create trillions of dollars in value in the process and outpace BTC growth”. Imagine that as a bet, but now instead it’s a 200-foot putt and if you make the putt you win billions of dollars. Like a carnival game, you have to pay $5 to attempt to make the putt, except with this game, the second time you try you pay $10, and the third $15, and so on. It’s a hard put to make, so you’re probably going to miss a lot. But what if you NEVER ran out of money? Eventually you make the putt. It might be the 3,000th attempted putt, but eventually you drain the 200-foot put and “other uses cases for crypto outside of holding BTC gains mass adoption, creates trillions of dollars in value in the process and outpaces BTC growth”. That’s what appears to be going on at the moment.

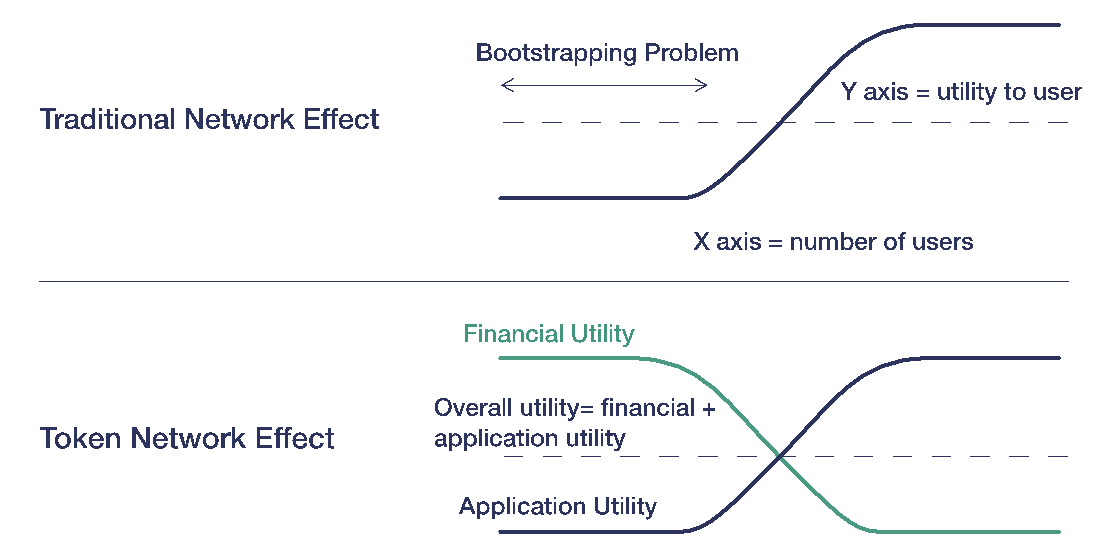

There’s a good chance the putt eventually gets drained. If enough capital is flowing in a manner that dictates a Multichain World, eventually it becomes self-fulfilling. The user growth isn’t there yet but the innovation will eventually lead to that. And the funding well will never run dry. It’s a setup that may very well set the course for the destiny of crypto to be a Multichain World, and sooner than would otherwise be the case. I certainly don’t want to come off as being against the experimentation and innovation happening with all the other use cases for DLT outside of Bitcoin. And I’m not saying I’m against the price being paid today for that experimentation and innovation, although that’s certainly a distinct topic worthy of examination. I’m reminded of a chart that I used to include in some of the first presentations I ever gave on crypto in 2018.

Source: Ikigai.

It’s a good one to emphasize that speculation drives adoption in crypto in a unique way that the world has not seen before. Financial utility literally pulls application utility into existence. Speculation serves a foundational purpose in crypto and it happens earlier in the life cycle of a company or project in crypto than ever before. That’s bound to cause some “funkiness” from time to time.

At some point, perhaps long after ETH or aggregate Layer 1’s have flipped BTC’s market cap, and the DeFi sector market cap has boomed and busted a few times, and other application layer market caps have boomed and busted a few times, the market may arrive at a different conclusion about non-BTC use cases. Friendly reminder - value did not accrue at the protocol layer in the buildout of the internet. The vast majority of internet users have literally no clue how it actually works. They are unaware of the protocols’ existence. There’s good reason to think crypto will eventually end up the same way – protocols creating all sorts of value via all sorts of use cases but with the nuts and bolts completely hidden away. This could have significant implications for value accrual in various sectors of crypto assets. The market may decide that ETH isn’t FAANG, its VOIP. That Layer 1’s aren’t Big Tech, they’re HTTP. And that Bitcoin isn’t gold. It’s US Treasuries, and those are worth $23tn and heading higher.

Source: FRED. As of 7/1/21.

The US dollar is the world reserve currency but US Treasuries are the foundation of the global financial system. Treasuries are currently the “pristine collateral” upon which all credit flows and all interest rates are set. If the global financial system slowly deems Bitcoin as pristine collateral in the coming decade because it has characteristics that deem it worthy of being pristine collateral relative to alternatives, Bitcoin Dominance may end up in a much higher spot than Multichain World investors are currently betting on. It would still be a Multichain World, but Bitcoin would be wrapped and sent cross-chain to the far corners of the crypto universe, while retaining more relative value. That’s a world where the market has decided pristine collateral is where more value will accrue because of the assignment of a monetary premium based on “moneyness” characteristics rather than innovation. In that world Layer 1’s are simply protocols – rails to transfer value that mostly accrues elsewhere.

It’s an outcome that could certainly happen. But to be honest it looks like the pendulum will swing in the opposite direction in the near-term – towards a low-Dominance, Multichain World. That low-Dominance might reverse course temporarily as loose monetary and fiscal policy abates, but it will be back stronger than ever when that looseness and the accompanying risk appetite it engenders returns. To paraphrase Field of Dreams, “if you build it and keeping building it and never run out of money and the hunt for outsized returns remains fierce, eventually they will come”.

Market Update – Liquid Crypto Asset Investing

| Symbol | August | July | QTD | Q2-21 | Q1-21 | YTD | 2020 | 2019 |

|---|---|---|---|---|---|---|---|---|

| BTC | 13% | 19% | 35% | -41% | 103% | 63% | 303% | 92% |

| ETH | 35% | 12% | 51% | 19% | 160% | 365% | 469% | -3% |

| XRP | 59% | 6% | 68% | 23% | 161% | 441% | 14% | -45% |

| BCH* | 16% | 2% | 19% | -11% | 45% | 53% | 71% | 30% |

| EOS | 23% | -1% | 22% | -14% | 85% | 94% | 1% | 0% |

| BNB | 39% | 10% | 53% | 0% | 708% | 1143% | 172% | 123% |

| XTZ | 70% | 0% | 70% | -37% | 142% | 157% | 49% | 192% |

| XLM | 19% | 1% | 20% | -31% | 220% | 165% | 184% | -60% |

| LTC | 18% | 1% | 19% | -27% | 58% | 38% | 202% | 36% |

| TRX | 39% | -6% | 30% | -26% | 244% | 231% | 101% | -29% |

| Aggregate Mkt Cap | 27% | 14% | 45% | -23% | 146% | 174% | 301% | 51% |

| Aggregate DeFi* | 37% | 32% | 81% | -27% | 339% | 485% | 1177% | 77% |

| Aggr Alts Mkt Cap | 40% | 9% | 53% | 1% | 246% | 435% | 274% | -1% |

Source: CoinMarketCap. As of 8/31/21. BCH includes SV. Aggregate DeFi from Coingecko.

Bitcoin was up 13% in August and resumed its trend of underperformance vs ETH and most Alts that has dominated YTD. BTC’s +63% YTD performance looks pathetic against many other names – ETH +365%, aggregate Alts +435% and aggregate DeFi +485%. 2021 has been a Multichain World.

Granted, it took King Bitcoin finding a firm bottom in late July before ETH and Alts broadly really started taking off, but once it did, Alts were off to the races. The market’s insistence on pricing in a Multichain World in August persisted despite stiff language from SEC Chairman Gensler around DeFi and despite the growing expectation that we will have a 40 Act BTC CME Futures ETF approved in less than two months. The London Hard Fork came and went, ETHBTC consolidated for four weeks, and now appears to be breaking out - with cyclical highs within close reach and new ATH’s not out of the picture. Gensler be damned, the market wants to buy FAANG.

Source: TradingView. As of 8/31/21.

What we learned over the last several months is that Bitcoin needs to be reasonably stable for a Multichain World to continue to be aggressively priced in. If Bitcoin had indeed broken down from the $30k level, I’m confident ETH would have underperformed BTC, and most Alts would have underperformed ETH. Instead, BTC is currently in a much healthier spot than it was a month ago and a MUCH healthier spot than two months ago. I’ve been showing the chart below for months now. I was worried about how much technical damage had been done to the BTC chart. An incredible amount of that has been repaired since July 20th.

Source: TradingView. As of 8/31/21.

Note the weekly MACD flip below and subsequent follow through. This looks like a chart that wants $58k at least. There’s a decent chance we slice through ATH’s with relative ease.

Source: TradingView. As of 8/31/21.

A 40 Act Bitcoin CME Futures ETF approval is a significant and straightforward catalyst that could easily be enough to take us near ATHs if not beyond. Should those ETFs get denied for any reason, that would likely prove damaging to Bitcoin price in the near-term. The other large risk is the Fed beginning to taper in the coming months. This was a much bigger risk before Jackson Hole, but reading the tea leaves of Powell and other committee members’ comments, it appears there is enough risk around Delta Variant, enough slack in the labor market, and weak enough sustainable increases in inflation that tapering has been punted to year-end if not into 2022. This should be a green light for Bitcoin specifically and crypto broadly in the coming months. Should the jobs numbers meaningfully surprise to the upside in the next two months, this would bring forward tapering fears and could put the lid on crypto prices near-term. There’s a good chance this pullback, should it occur, would be accompanied by a rise in Dominance, but I’m not certain of it. Earlier tapering is not my base case anyway. The Fed will probably let things run hot for another few months at least.

Bitcoin open interest is elevated but still way off its highs and lower than it was when price was at these levels two times prior this year. There’s leverage in this market for sure, but it’s not egregious.

Source: Bybt. As of 8/31/21.

This is less true for ETH at the moment than for BTC. Open Interest is elevated.

Source: Bybt. As of 8/31/21.

Spot Bitcoin volumes are currently at the lowest levels since mid-October, right before Bitcoin went on an absolute tear.

Source: TradingView. As of 8/31/21.

Bitcoin price volatility, as measured by 4hr Bollinger Band width, is coiled. A violent move in one direction or another is likely brewing, perhaps in September. My gut right now says that will be to the upside, but I’ve been wrong before.

Source: TradingView. As of 8/31/21.

Overall, the market seems intent on funding a Multichain World, so long as Bitcoin is safe. Bitcoin looks pretty safe right now, so the horizontal expansion of a Multichain World will likely continue. Should a 40 Act BTC ETF approval become increasingly apparent in the coming weeks, I would expect that to be good for a Dominance bounce that could last a few days or a few weeks or maybe a month. But I would guess that relatively quickly, the increase in BTC relative market cap would just serve to further embolden capital to flow elsewhere, out of BoomerCoin and into something with a bit more juice in it.

Closing Remarks

It is notable, at least to myself, that the message of this Monthly Update letter is a meaningful departure from the stance I’ve generally had here over the last three years. Ikigai’s investment strategy has been Bitcoin-centric for the last two years. Through a models-driven, quantamental approach, we figured out a way to outperform just holding Bitcoin, mostly through trading Bitcoin and without using much leverage. We decided to focus on Bitcoin because it was big, it was liquid, it had a proven and compelling use case, it makes the world a better place, and it generated quantitative data we believed gave us clear and consistent edge through a full crypto cycle. We could have just put the whole fund in ETH and played golf for three years instead. That’s not exactly risk management and hindsight is 20/20 for sure, but with the thousands of hours I’ve poured into this work over the last few years, that point is not lost on me.

I’ve said it many times before, but there are many use cases for DLT. When evaluating these various use cases, we ask ourselves four questions:

How ready is the world for the tech?

How ready is the tech for the world?

What do you need decentralization for?

How decentralized is decentralized enough?

We believed BTC much more fully and convincingly answered those four questions than any other crypto asset in existence. We’ve also explicitly highlighted value creation vs value accrual, and those two things being different from one another, and the bridge between value creation and value accrual being token structure. We believed Bitcoin had a more compelling token structure than any other crypto asset.

Do we still think those four questions are valid? We do. Do we still believe Bitcoin has the most complete answers to those questions? We do. Do we still believe Bitcoin compellingly accrues the value it creates? We do. But you can’t just take that in a vacuum and ignore everything else. Other factors have changed. The ever-subjective process of value assignment has evolved for all asset classes over the last few years. We are in the midst of the largest asset bubble in human history, driven by the largest monetary experiment in human history. This has caused changes in risk-taking behavior that trickle out to every corner of the market. One trickle-down effect has been the strength of the market’s desire to see crypto become a Multichain World. We plan to act accordingly.

“Be not afraid of going slowly. Be afraid of standing still.”

– Japanese Proverb

Travis Kling

Founder & Chief Investment Officer

Ikigai Asset Management

P.S.

Included below is an incomplete list of memorable tweets from the last month. Twitter is not investment advice and my views could easily be wrong. That being said, like it or not, Twitter matters for crypto. I have no interest in being a talking head for a living and babbling about on Twitter is a long way away from being a good steward of investor capital. However, this is a community with open-source software in its DNA, and participants want to crowd-source the truth. We are shepherds of this technology. Answers to fundamental questions about this asset class are not currently clear, so having a public platform to share your views with the community is important. After all, you’re helping shape the future :)

1. Ikigai Asset Management is the trade name for a collection of advisory and consulting businesses operated by Travis Kling, Anthony Emtman, and their team.

The information contained or attached herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. This presentation may contain forward-looking statements that are within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements are based on management’s beliefs, as well as assumptions made by, and information currently available to, management. Although management believes that the expectations reflected in these forward-looking statements are reasonable, it can give no assurance that these expectations will prove to be correct. This email is for informational purposes only and does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product, service of Ikigai as well as any Ikigai fund, whether an existing or contemplated fund, for which an offer can be made only by such fund’s Confidential Private Placement Memorandum and in compliance with applicable law. Past performance is not indicative nor a guarantee of future returns. Please consult your own independent advisors. All information is intended only for the named recipient(s) above and is covered by the Electronic Communications Privacy Act 18 U.S.C. Section 2510-2521. This email is confidential and may contain information that is privileged or exempt from disclosure under applicable law. If you have received this message in error please immediately notify the sender by return email and delete this email message from your computer. Copyright 2021 Ikigai Asset Management, LLC. All Rights Reserved.

NOT INVESTMENT ADVICE; FOR INFORMATION ONLY

PAST PERFORMANCE IS NOT A GUARANTEE OF FUTURE RESULTS